Ministry of Finance

SUMMARY OF ECONOMIC SURVEY 2024-25

प्रविष्टि तिथि:

31 JAN 2025 2:23PM by PIB Delhi

INDIA’S GDP EXPECTED TO GROW BETWEEN 6.3 & 6.8 PER CENT IN FY26

REAL GDP ESTIMATED AT 6.4 PER CENT IN FY25, CLOSE TO ITS DECADAL AVERAGE

REAL GVA ESTIMATED TO GROW BY 6.4 PER CENT IN FY25

CAPEX GROWS AT 8.2 PER CENT IN JULY – NOVEMBER 2024 AND EXPECTED TO PICK UP FURTHER PACE

RETAIL HEADLINE INFLATION SOFTENED TO 4.9 PER CENT IN APRIL-DECEMBER 2024

INDIA’S CONSUMER PRICE INFLATION TO ALIGN WITH THE TARGET OF AROUND 4 PER CENT IN FY26

OVERALL EXPORTS GROW 6.0 PER CENT (YOY) DURING APRIL-DECEMBER 2024

INDIA’S SERVICES EXPORT GROWTH SURGED TO 12.8 PER CENT DURING APRIL–NOVEMBER FY25, UP FROM 5.7 PER CENT IN FY24

GROSS FDI INFLOWS INCREASE FROM USD 47.2 BILLION IN FIRST EIGHT MONTHS OF FY24 TO USD 55.6 BILLION IN THE SAME PERIOD OF FY25, A YOY GROWTH OF 17.9 PER CENT

FOREX AT USD 640.3 BILLION AS OF END OF DECEMBER 2024, SUFFICIENT TO COVER 10.9 MONTHS OF IMPORTS AND APPROXIMATELY 90 PER CENT OF EXTERNAL DEBT

CAPACITY ADDITION IN SOLAR AND WIND POWER INCREASES 15.8 PER CENT YEAR-ON-YEAR IN DECEMBER 2024

BSE STOCK MARKET CAPITALISATION TO GDP RATIO AT 136 PER CENT AT THE END OF DECEMBER 2024, FAR HIGHER THAN CHINA (65 PER CENT) AND BRAZIL (37 PER CENT)

ECONOMIC SURVEY ADVOCATES DEREGULATION TO ACCELERATE AND SUSTAIN ECONOMIC GROWTH

CONTINUED STEP-UP OF INFRASTRUCTURE INVESTMENT OVER NEXT TWO DECADES NEEDED TO SUSTAIN A HIGH GROWTH

₹50,000 CRORE SELF-RELIANT INDIA FUND LAUNCHED TO PROVIDE EQUITY FUNDING TO MSMES

AGRICULTURE EXPECTED TO GROW AT 3.8 PER CENT IN FY25

KHARIF FOODGRAIN PRODUCTION FOR 2024 IS EXPECTED TO REACH 1647.05 LMT, AN INCREASE OF 89.37 LMT OVER PREVIOUS YEAR

KEY DRIVERS OF AGRICULTURAL GROWTH ARE HORTICULTURE, LIVESTOCK & FISHERIES

INDUSTRIAL SECTOR ESTIMATED TO GROW BY 6.2 PER CENT IN FY25

SOCIAL SERVICES EXPENDITURE REGISTERS AN ANNUAL GROWTH RATE OF 15 PER CENT BETWEEN FY 21 AND FY 25

GOVERNMENT HEALTH EXPENDITURE INCREASES FROM 29.0 PER CENT TO 48.0 PER CENT; SHARE OF OUT OF POCKET EXPENDITURE IN TOTAL HEALTH EXPENDITURE DECLINES FROM 62.6 PER CENT TO 39.4 PER CENT BETWEEN FY15 AND FY22

UNEMPLOYMENT RATE DECLINES TO 3.2 PER CENT IN 2023-24 (JULY-JUNE) FROM 6.0 PER CENT IN 2017-18 (JULY-JUNE)

COLLABORATIVE EFFORT BETWEEN GOVERNMENT, PRIVATE SECTOR, AND ACADEMIA ESSENTIAL TO MINIMISE ADVERSE AI SOCIETAL EFFECTS

“The global economy grew by 3.3 per cent in 2023. The International Monetary Fund (IMF) projects global growth to average around 3.2 per cent over the next five years, which is modest by historical standards”, says the Economic Survey 2024-25 tabled by Union Minister of Finance and Corporate Affairs Smt. Nirmala Sitharaman, in the Parliament today.

As per the Survey, the global economy exhibited steady yet uneven growth across regions in 2024. A notable trend was the slowdown in global manufacturing, especially in Europe and parts of Asia, due to supply chain disruptions and weak external demand. In contrast, the services sector performed better, supporting growth in many economies. Inflationary pressures eased in most economies. However, services inflation has remained persistent, notes the Survey.

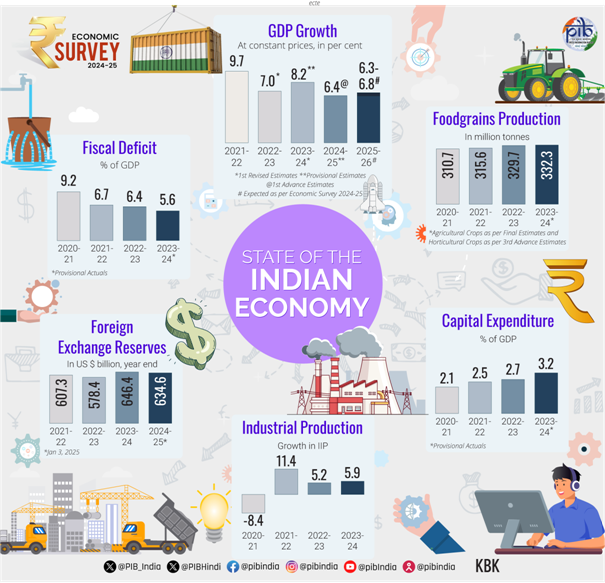

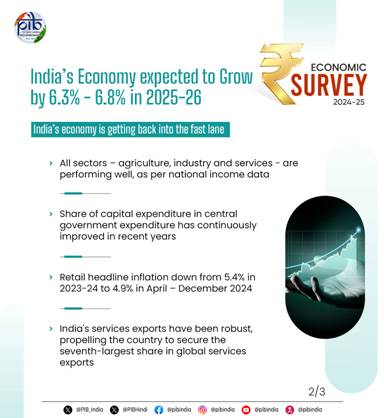

The Survey highlights that, despite global uncertainty, India has displayed steady economic growth. India's real GDP growth of 6.4 per cent in FY25 remains close to the decadal average.

From an aggregate demand perspective, private final consumption expenditure at constant prices is estimated to grow by 7.3 per cent, driven by a rebound in rural demand.

On the supply side, the real gross value added (GVA) is estimated to grow by 6.4 per cent. The agriculture sector is expected to rebound to a growth of 3.8 per cent in FY25. The industrial sector is estimated to grow by 6.2 per cent in FY25. Strong growth rates in construction activities and electricity, gas, water supply and other utility services are expected to support industrial expansion. Growth in the services sector is expected to remain robust at 7.2 per cent, driven by healthy activity in financial, real estate, professional services, public administration, defence, and other services.

Keeping in mind the upsides and downsides to growth, the Survey expects the real GDP growth in FY26 to be between 6.3 and 6.8 per cent.

The Chapter on the Medium-Term Outlook elaborates on the global factors and the importance of strengthening the levers of domestic growth in the context of heightened risks due to global concerns about economic policies and trade policy uncertainties.

To realize the aspirations of Viksit Bharat by 2047, it is important that the medium-term growth outlook of India be assessed in the context of emerging global realities of Geo-Economic Fragmentation (GEF), Chinese manufacturing prowess, and global dependency on China for energy transition efforts. The Survey puts forth a way forward to reinvigorate the internal engines and domestic levers of growth by focusing on one central element of systemic deregulation, which will enable a paradigm of economic freedom to businesses of individuals and organizations to pursue legitimate economic activity with ease. The Survey stresses that the reforms and economic policy must now be on systematic deregulation under Ease of Doing Business 2.0 so that it encourages creation of a viable Mittelstand, i.e. India’s SME sector.

The Economic Survey 2024-25 notes that agriculture growth remained steady in first half of FY25, with Q2 recording a growth rate of 3.5 per cent, marking an improvement over the previous four quarters. Healthy Kharif production, above-normal monsoons, and an adequate reservoir level supported agricultural growth. The total Kharif food grain production is estimated at a record 1647.05 lakh metric tonnes (LMT) in 2024-25, higher by 5.7 per cent compared to 2023-24 and 8.2 per cent higher than the average food grain production in the past five years.

The industrial sector grew by 6 per cent in first half of FY25, and is estimated to grow by 6.2 per cent in FY25. Q1 saw a strong growth of 8.3 per cent, but growth moderated in Q2 due to three key factors. First, manufacturing exports slowed significantly due to weak demand from destination countries, and aggressive trade and industrial policies in major trading nations. Second, the above average monsoon had mixed effects - while it replenished reservoirs and supported agriculture, it also disrupted sectors like mining, construction, and, to some extent, manufacturing. Third, the variation in the timing of festivities between September and October in the previous and current years led to a modest growth slowdown in Q2 FY25.

Despite various challenges, India continues to register the fastest growth in manufacturing PMI, stated the Survey. The latest Manufacturing PMI for December 2024 remained well within the expansionary zone, driven by new business gains, robust demand, and advertising efforts.

The services sector continues to perform well in FY25, emphasizes the Survey. A notable growth in Q1 and Q2 resulted in 7.1 per cent growth in first half of FY25. Across sub-categories, all the sub-sectors have performed well. India’s services export growth surged to 12.8 per cent during April–November FY25, up from 5.7 per cent in FY24.

The Economic Survey states that growth process has been ably supported by stability on fronts such as inflation, fiscal health, and external sector balance. On inflation, the Survey states that retail headline inflation has softened from 5.4 per cent in FY24 to 4.9 per cent in April – December 2024. Food inflation, measured by the Consumer Food Price Index (CFPI), has increased from 7.5 per cent in FY24 to 8.4 per cent in FY25 (April-December), primarily driven by a few food items such as vegetables and pulses. India’s consumer price inflation will gradually align with the target of around 4 per cent in FY26 as per RBI and IMF.

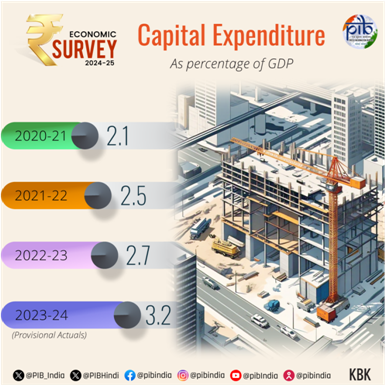

Capital expenditure (capex), as a per cent of the total expenditure of the union, has continuously improved from FY21 to FY24. After the general elections, union government capex has grown by 8.2 per cent during July – November 2024 YoY, the Survey says.

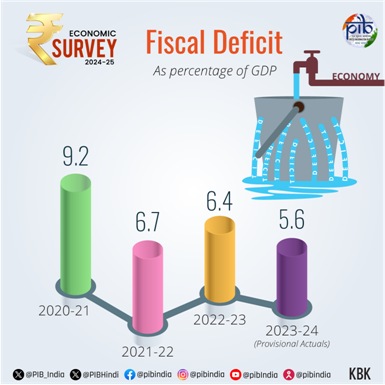

Despite the gross tax revenue (GTR) increasing by 10.7 per cent YoY during April-November 2024, the tax revenue retained by the Union, net of devolution to the states, hardly increased, says the Survey. As of November, the deficit indicators of the union were comfortably placed, leaving ample room for developmental and capital expenditure in the rest of the year.

According to the Survey, the GTR of the union and own tax revenue (OTR) of the states have increased at comparable pace during the period April - November 2024. The revenue expenditure of the states grew at 12 per cent (YoY) during April to November 2024, with subsidies and committed liabilities registering a growth of 25.7 per cent and 10.4 per cent, respectively.

The Survey observes that stability in the banking sector is underscored by declining asset impairments, robust capital buffers, and strong operational performance. The gross non-performing assets (NPAs) in the banking system have declined to a 12-year low of 2.6 per cent of gross loans and advances. The capital-to-risk-weighted assets ratio (CRAR) for Schedule Commercial Banks stands at 16.7 per cent as of September 2024, well above the norm, says the Survey.

Emphasizing that the external sector stability is safeguarded by services trade and record remittances, the Economic Survey quotes that India’s merchandise exports grew by 1.6 per cent YoY in April – December 2024. Merchandise imports rose by 5.2 per cent. India's robust services exports have propelled the country to secure the seventh-largest share in global services exports, underscoring its competitiveness.

In addition to the services trade surplus, remittances from abroad led to a healthy net inflow of private transfers. India was the top recipient of remittances in the world, driven by an uptick in job creation in OECD economies. These two factors combined to ensure that India’s current account deficit (CAD) remains relatively contained at 1.2 per cent of GDP in Q2 FY25, as per the Survey.

Gross Foreign Direct Investment inflows recorded a revival in FY25, increasing from USD 47.2 billion in the first eight months of FY24 to USD 55.6 billion in the same period of FY25, a YoY growth of 17.9 per cent, says the Survey. Foreign portfolio investment (FPI) flows have been volatile in the second half of 2024, primarily on account of global geopolitical and monetary policy developments.

The Economic Survey states that as a result of stable capital flows, India’s foreign exchange reserves increased from USD 616.7 billion at the end of January 2024 to USD 704.9 billion in September 2024 before moderating to USD 634.6 billion as on 3 January 2025. India’s forex reserves are sufficient to cover 90 per cent of external debt and provide an import cover of more than ten months, thereby safeguarding against external vulnerabilities.

The Economic Survey highlights continued good performance on the employment front. It states that India's labour market growth in recent years has been supported by post-pandemic recovery and increased formalisation. The unemployment rate for individuals aged 15 years and above has steadily declined from 6 per cent in 2017-18 to 3.2 per cent in 2023-24. The labour force participation rate (LFPR) and the worker-to-population ratio (WPR) have also increased.

The Survey also mentions that for India, a services-driven economy with a youthful and adaptable workforce, the adoption of AI offers the potential to support economic growth and improve labour market outcomes. Prioritising education and skill development will be crucial to equipping workers with the competencies needed to thrive in an AI-augmented landscape. The Survey brings out the fact that there are at present barriers to large-scale AI adoption, leading to a window for policymakers to act. The Economic Survey calls upon for collaborative effort between government, private sector, and academia to minimise the adverse societal effects of AI-driven transformation in the labour sector.

On infrastructure front, the Economic Survey highlights the need for continued step-up of infrastructure investment over next two decades to sustain a high growth. Under railway connectivity, 2031 km of railway network was commissioned between April and November, 2024, and 17 new pairs of Vande Bharat trains were introduced between April and October 2024. Port capacity improved significantly in FY25, leading to improvements in operational efficiency and reduction in average container turnaround time in major ports from 48.1 hours in FY24 to 30.4 hours during FY25 (Apr-Nov).

The Economic Survey underscores the government of India’s efforts to boost renewable energy in the country and green investments through schemes, policies, financial incentives and regulatory measures such as PM - Surya Ghar: Muft Bijli Yojana, National Bioenergy Programme, National Green Hydrogen Mission and PM-KUSUM. The capacity addition in solar and wind power has lead to a 15.8 per cent year-on-year increase in renewable energy capacity by December 2024.

The Government social services expenditure has witnessed an increase of compounded annual growth rate of 15% (combined for centre and states) from FY 21 to FY 25. The Gini coefficient, which is a measure of inequality in consumption expenditure, has been declining in recent years (For rural areas it declined to 0.237 in 2023-24 from 0.266 in 2022-23 and for urban areas, it fell to 0.284 in 2023-24 from 0.314 in 2022-23), reflecting positive impact of Government’s initiatives in reshaping income distribution. On the school education front, the government is working toward meeting the objectives of National Education Policy 2020 through a range of programmes and schemes. These interalia include the Samagra Shiksha Abhiyan, DIKSHA, STARS, PARAKH, PM SHRI, ULLAS, PM POSHAN, etc, as per the Survey.

In the total health expenditure of the country between FY15 and FY22, the Survey quotes the share of government health expenditure has increased from 29.0 per cent to 48.0 per cent. During the same period, the share of out-of-pocket expenditure in total health expenditure declined from 62.6 per cent to 39.4 per cent.

Micro, Small and Medium Enterprises (MSME) sector has emerged as a highly vibrant sector of the Indian economy, noted the Survey. To provide equity funding to MSMEs with the potential to scale up, the government launched the Self-Reliant India Fund with a corpus of ₹50,000 crore.

The Survey, says that reducing excessive regulatory burdens, governments can help businesses become more efficient, reduce costs, and unlock new growth opportunities. Regulations increase the cost of all operational decisions in firms, the Economic Survey adds. It has outlined a three-step process for states to systematically review regulations for their cost-effectiveness. The steps include identifying areas for deregulation, thoughtfully comparing the regulations with other states and countries and estimating the cost of each of these regulations on individual enterprises. The Survey highlights that Ease of Doing Business (EoDB) 2.0 should be a state government-led initiative focused on fixing the root causes behind the unease of doing business. It mentions that in the next phase for EoDB, states must break new ground on liberalizing standards and controls, setting legal safeguards for enforcement, reducing tariffs and fees, and applying risk-based regulation.

As the Survey underscores, looking ahead, India’s economic prospects for FY26 are balanced. Headwinds to growth include elevated geopolitical and trade uncertainties and possible commodity price shocks. Domestically, the translation of order books of private capital goods sector into sustained investment pick-up, improvements in consumer confidence, and corporate wage pick-up will be key to promoting growth. Rural demand backed by a rebound in agricultural production, an anticipated easing of food inflation and a stable macro-economic environment provides an upside to near-term growth. Overall, India will need to improve its global competitiveness through grassroots-level structural reforms and deregulation to reinforce its medium-term growth potential.

*****

NB/RC/AG/GS

(रिलीज़ आईडी: 2097921)

आगंतुक पटल : 135957

इस विज्ञप्ति को इन भाषाओं में पढ़ें:

Odia

,

Urdu

,

Tamil

,

Malayalam

,

Kannada

,

Bengali

,

हिन्दी

,

Nepali

,

Assamese

,

Punjabi

,

Gujarati

,

Telugu