Ministry of Finance

Pradhan Mantri Jan Dhan Yojana (PMJDY) - National Mission for Financial Inclusion, completes eight years of successful implementation

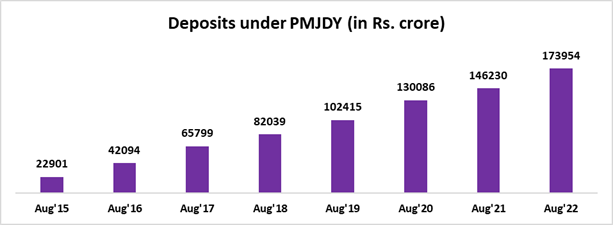

More than 46.25 crore beneficiaries banked under PMJDY since inception, amounting to Rs. 1,73,954 crore

FM Smt. Nirmala Sitharaman: Financial inclusion is a major step towards inclusive growth which ensures overall economic development of marginalised sections of society

PMJDY has become the foundation stone for the government's people-centric economic initiatives: MoS Finance, Dr. Bhagwat Karad

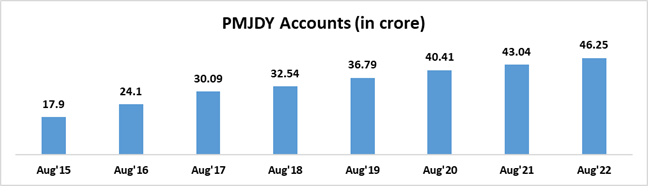

PMJDY Accounts grow 3-fold from 14.72 crore in Mar’15 to 46.25 crore as on 10-08-2022

56% Jan-Dhan account holders are women and 67% Jan Dhan accounts in rural and semi-urban areas

31.94 crore RuPay cards issued to PMJDY accountholders

About 5.4 crore PMJDY account holders received direct benefit transfer (DBT) from the Government under various schemes in June, 2022

प्रविष्टि तिथि:

28 AUG 2022 7:40AM by PIB Delhi

The Ministry of Finance, through its financial inclusion led interventions, is committed to provide financial inclusiveness and support to the marginalised and hitherto socio-economically neglected classes. Through Financial Inclusion (FI) we can achieve equitable and inclusive growth of the nation. Financial Inclusion stands for delivery of appropriate financial services at an affordable cost, on timely basis to vulnerable groups such as low-income groups and weaker sections who lack access to even the most basic banking services.

It is important as it provides an avenue to the poor for bringing their savings into the formal financial system, an avenue to remit money to their families in villages besides taking them out of the clutches of the usurious money lenders. A key initiative towards this commitment is the Pradhan Mantri Jan Dhan Yojna (PMJDY), which is one of the biggest financial inclusion initiatives in the world.

PMJDY was announced by Prime Minister, Shri Narendra Modi in his Independence Day address on 15th August 2014. While launching the programme on 28th August, the Prime Minister had described the occasion as a festival to celebrate the liberation of the poor from a vicious cycle.

On the occasion 8th Anniversary of PMJDY, Union Finance Minister Smt. Nirmala Sitharaman in her message said that. “Financial inclusion is a major step towards inclusive growth which ensures the overall economic development of the marginalised sections of the society. The success of the PMJDY since August 28, 2014 is reflected in terms of opening of over 46 crore bank accounts with deposit balance of Rs 1.74 lakh crore with its expanded coverage to 67% rural or semi-urban areas as well as 56% of women Jan Dhan account holders. Continuation of PMJDY beyond 2018 saw a marked shift in approach to meet challenges and requirements of emerging FI landscape in the country. There has been a shift in focus from “every household’ to “every adult”, with added emphasis on usage of accounts by enhancing Direct Benefit Transfer (DBT) flows through these accounts, promoting digital payments through the use of RuPay cards, etc, She added.”

“The underlying pillars of PMJDY, namely, Banking the Unbanked, Securing the Unsecured and Funding the Unfunded has made it possible to adopt multi-stakeholders’ collaborative approach while leveraging technology for serving the unserved and underserved areas as well,” the Finance Minister said.

The Finance Minister further stated in her message that, “The JAM pipeline created through account holders’ consent-based linking of bank accounts with Aadhar and mobile numbers of the account holders, which is one of the important pillars of FI ecosystem, has enabled instant DBT under various government welfare schemes to the eligible beneficiaries. The advantage of the architecture created under FI ecosystem came handy during the Covid-19 pandemic when it facilitated direct income support to farmers under PM-KISAN and transfer of ex-gratia payment to women PMJDY account holders under PMGKP in a seamless and time-bound manner.

Smt. Sitharaman concluded her message and said, “Financial Inclusion needs policy-led intervention based on an architecture linked to suitable financial products, information and communication technologies and data infrastructure. The country has adopted this strategy since the launch of PMJDY to optimise the intended benefits of the scheme for the people of the country. I thank all the field functionaries for their untiring efforts in making PMJDY a grand success.

Expressing his thoughts for PMJDY on this occasion, Union Minister of State for Finance Dr. Bhagwat Karad said, “Pradhan Mantri Jan Dhan Yojana (PMJDY) has been one of the most far reaching initiatives towards Financial Inclusion not only in India but in the world. Financial Inclusion is among top-most priorities of the Government as it is an enabler for inclusive growth. It provides an avenue to the poor for bringing their savings into the formal financial system, an avenue to remit money to their families besides taking them out of the clutches of the usurious money lenders.”

Dr Karad said, “On the 8th Anniversary of PMJDY, the importance of this Scheme is reiterated. PMJDY has become the foundation stone for the government's people-centric economic initiatives. Whether it is direct benefit transfers, COVID-19 financial assistance, PM-KISAN, increased wages under MGNREGA, life and health insurance cover, the first step is to provide every adult with a bank account, which PMJDY has nearly completed.”

“I am confident that banks will rise to the occasion and contribute to this national endeavour in significant measure and re-dedicate your selves to ensure that each and every adult is covered under the Financial Inclusion initiatives of the government,” Dr Karad said.

As we complete 8 years of successful implementation of this Scheme, we take a look at the major aspects and achievements of this Scheme so far.

Background

Pradhan Mantri Jan Dhan Yojana (PMJDY) is National Mission for Financial Inclusion to ensure access to financial services, namely, Banking/ Savings & Deposit Accounts, Remittance, Credit, Insurance, Pension in an affordable manner.

- Objectives:

- Ensure access of financial products & services at an affordable cost

- Use of technology to lower cost & widen reach

- Basic tenets of the scheme

- Banking the unbanked - Opening of basic savings bank deposit (BSBD) account with minimal paperwork, relaxed KYC, e-KYC, account opening in camp mode, zero balance & zero charges

- Securing the unsecured - Issuance of Indigenous Debit cards for cash withdrawals & payments at merchant locations, with free accident insurance coverage of Rs. 2 lakh

- Funding the unfunded - Other financial products like micro-insurance, overdraft for consumption, micro-pension & micro-credit

- Initial Features

The scheme was launched based upon the following 6 pillars:

- Universal access to banking services – Branch and BC

- Basic savings bank accounts with overdraft facility of Rs. 10,000/- to every eligible adult

- Financial Literacy Programme– Promoting savings, use of ATMs, getting ready for credit, availing insurance and pensions, using basic mobile phones for banking

- Creation of Credit Guarantee Fund – To provide banks some guarantee against defaults

- Insurance – Accident cover up to Rs. 1,00,000 and life cover of Rs. 30,000 on account opened between 15 Aug 2014 to 31 January 2015

- Pension scheme for Unorganized sector

- Important approach adopted in PMJDY based on past experience:

-

- Accounts opened are online accounts in core banking system of banks, in place of earlier method of offline accounts opening with technology lock-in with the vendor

- Inter-operability through RuPay debit card or Aadhaar enabled Payment System (AePS)

- Fixed-point Business Correspondents

- Simplified KYC / e-KYC in place of cumbersome KYC formalities

- Extension of PMJDY with New features – The Government decided to extend the comprehensive PMJDY programme beyond 28.8.2018 with some modifications

v Focus shift from ‘Every Household’ to Every Unbanked Adult’

v RuPay Card Insurance - Free accidental insurance cover on RuPay cards increased from Rs. 1 lakh to Rs. 2 lakh for PMJDY accounts opened after 28.8.2018.

v Enhancement in overdraft facilities -

- OD limit doubled from Rs 5,000/- to Rs 10,000/-; OD upto Rs 2,000/- (without conditions).

- Increase in upper age limit for OD from 60 to 65 years

- Impact of PMJDY

PMJDY has been the foundation stone for people-centric economic initiatives. Whether it is direct benefit transfers, COVID-19 financial assistance, PM-KISAN, increased wages under MGNREGA, life and health insurance cover, the first step of all these initiatives is to provide every adult with a bank account, which PMJDY has nearly completed.

One in 2 accounts opened between Mar’14 to Mar’20 was a PMJDY account. Within 10 days of nationwide lockdown more than about 20 crore women PMJDY accounts were credited with ex-gratia.

Jandhan provides an avenue to the poor for bringing their savings into the formal financial system, an avenue to remit money to their families in villages besides taking them out of the clutches of the usurious money lenders. PMJDY has brought the unbanked into the banking system, expanded the financial architecture of India and brought financial inclusion to almost every adult.

In today's COVID-19 times, we have witnessed the remarkable swiftness and seamlessness with which Direct Benefit Transfer (DBTs) have empowered and provided financial security to the vulnerable sections of society. An important aspect is that DBTs via PM Jan Dhan accounts have ensured every rupee reaches its intended beneficiary and preventing systemic leakage.

- Achievements under PMJDY- As on 10th August’22:

- PMJDY Accounts

- As on 10th August ’22 number of total PMJDY Accounts: 46.25 crore; 55.59% (25.71 crore) Jan-Dhan account holders are women and 66.79% (30.89 crore) Jan Dhan accounts are in rural and semi-urban areas

- During first year of scheme 17.90 crore PMJDY accounts were opened

- Continuous increase in no of accounts under PMJDY

- PMJDY Accounts have grown three-fold from 14.72 crore in Mar’15 to 46.25 crore as on 10-08-2022. Undoubtedly a remarkable journey for the Financial Inclusion Programme.

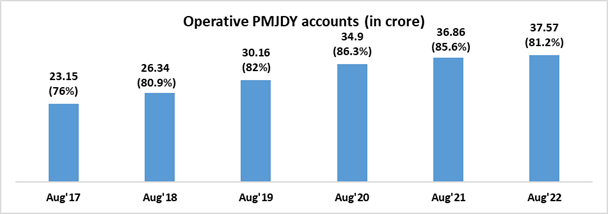

- Operative PMJDY Accounts –

- Deposits under PMJDY accounts –

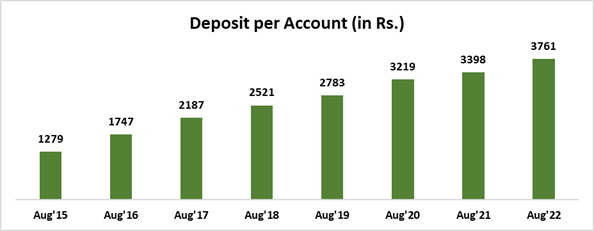

- Average Deposit per PMJDY account –

- Average deposit per account is Rs. 3,761

- Avg. Deposit per account has increased over 2.9 times over Aug’15

- Increase in average deposit is another indication of increased usage of accounts and inculcation of saving habit among account holders

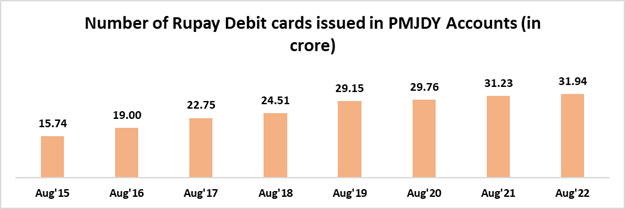

- Rupay Card issued to PMJDY account holders

- Total RuPay cards issued to PMJDY accountholders: 31.94 crore

- Number of RuPay cards & their usage has increased over time

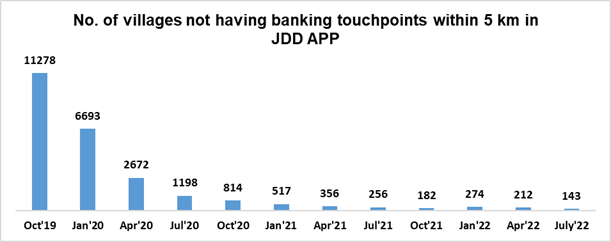

- Jan Dhan Darshak App

A mobile application, was launched to provide a citizen centric platform for locating banking touch points such as bank branches, ATMs, Bank Mitras, Post Offices, etc. in the country. Over 8 lakh banking touchpoints have been mapped on the GIS App. The facilities under Jan Dhan Darshak App could be availed as per the need and convenience of common people. The web version of this application could be accessed at the link http://findmybank.gov.in.

This app is also being used for identifying villages which are not served by banking touchpoints within 5 km. these identified villages are then allocated to various banks by concerned SLBCs for opening of banking outlets. The efforts have resulted in significant decrease in number of such villages.

- Towards ensuring smooth DBT transactions

As informed by banks, about 5.4 crore PMJDY accountholders receive direct benefit transfer (DBT) from the Government under various schemes.To ensure that the eligible beneficiaries receive their DBT in time, the Department takes active role in identification of avoidable reasons for DBT failures in consultation with DBT Mission, NPCI, banks and various other Ministries. With close monitoring in this regard through regular VCs with banks and NPCI, the share of DBT failures due to avoidable reasons as a percentage of total DBT failures has decreased from 13.5% (FY 19-20) to 9.7% (FY 21-22).

- Digital transactions: With the issue of over 31.94 crore RuPay debit cards under PMJDY, installation of 61.69 lakh PoS/mPoS machines as on June’22 and the introduction of mobile based payment systems like UPI, the total number of digital transactions have gone up from 978 crore in FY 2016-17 to 7,195 crore in FY 2021-22. The total number of UPI financial transactions have increased from 1.79 crore in FY 2016-17 to 4,596 crore in FY 2021-22. Similarly, total number of RuPay card transactions at PoS and E-commerce have increased from 28.28 crore in FY 2016-17 to 151.64 crore in FY 2021-22.

- The road ahead

- Endeavour to ensure coverage of PMJDY account holders under micro insurance schemes. Eligible PMJDY accountholders will be sought to be covered under PMJJBY and PMSBY. Banks have already been communicated about the same.

- Promotion of digital payments including RuPay debit card usage amongst PMJDY accountholders through creation of acceptance infrastructure across India

- Improving access of PMJDY account holders to Micro-credit and micro investment such as flexi-recurring deposit etc.

****

RM/MV/KMN

(रिलीज़ आईडी: 1854909)

आगंतुक पटल : 36354

इस विज्ञप्ति को इन भाषाओं में पढ़ें:

Urdu

,

Marathi

,

हिन्दी

,

Manipuri

,

Bengali

,

Assamese

,

Punjabi

,

Gujarati

,

Odia

,

Tamil

,

Telugu

,

Kannada

,

Malayalam