Ministry of Finance

ASSET QUALITY OF SCHEDULED COMMERCIAL BANKS (SCBs) WITNESSES SIGNIFICANT IMPROVEMENT, RECOVERY RATE IN NPAs APPROXIMATELY DOUBLES FROM 13.2 PER CENT IN FY18 TO 26.2 PER CENT IN FY25

RRBs ACHIEVE A RECORD CONSOLIDATED NET PROFIT OF ₹7.6 THOUSAND CRORE DURING FY24, FOLLOWED BY A SECOND-HIGHEST CONSOLIDATED NET PROFIT OF ₹6.8 THOUSAND CRORE DURING FY25

OVER ₹3.2 LAKH CRORE MSME LOAN APPLICATIONS, AMOUNTING TO MORE THAN ₹41.5 THOUSAND CRORE SANCTIONED BY PSBs UNDER THE CREDIT PROGRAMMES OF CREDIT ASSESSMENT MODEL, BETWEEN 1ST APRIL AND 30TH NOVEMBER 2025

ACTIVE BORROWERS IN MICROFINANCE SECTOR NEARLY DOUBLE FROM 330 LAKH IN FY14 TO 627 LAKH IN FY25; MFI BRANCH NETWORKS EXPAND FROM 11,687 BRANCHES TO 37,380 DURING THE SAME TIME

PMJDY OPENS 55.02 CRORE ACCOUNTS AS OF MARCH 2025, WITH 36.63 CRORE IN RURAL AND SEMI-URBAN AREAS; UPI BECOMES A FLAGSHIP SUCCESS STORY

UNDER IBC, CREDITORS RECOVER 94 PER CENT OF THE FAIR VALUE OF RESOLVED BUSINESSES; IBC ESTABLISHES A UNIFIED FRAMEWORK FOR RESOLVING CORPORATE DISTRESS IN INDIA, S&P UPGRADE INDIA’S GLOBAL RATINGS

प्रविष्टि तिथि:

29 JAN 2026 2:14PM by PIB Delhi

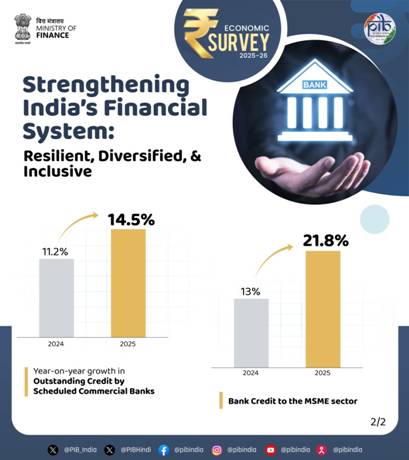

A significant improvement has been observed in the asset quality of Scheduled Commercial Banks (SCBs), states the Economic Survey 2025-26 that was tabled in the Parliament today by the Union Minister for Finance and Corporate Affairs Smt. Nirmala Sitharaman.. The gross non-performing asset (GNPA) ratio and net NPA ratio have reached a multi-decadal low level and record low level, respectively. At the same time, the capital-to-risk-weighted-asset ratio (CRAR) of the SCBs remained strong at 17.2 per cent as of September 2025.Further, the recovery rate in NPAs in SCBs has approximately doubled from 13.2 per cent in FY18 to 26.2 per cent in FY25. The recovery rate through the Insolvency and Bankruptcy Code, 2016 (IBC Code) has improved significantly as well.

Furthermore, measures announced in the Union Budget 2025-26, such as a significant enhancement of credit availability with guarantee cover for MSMEs, the introduction of credit cards for micro-enterprises, and others, have also been beneficial to the sector. The revision in MSMEs classification, wherein investment limits and turnover thresholds have been substantially raised, also contributed to this high growth. The bank credit to the MSME sector continues to show momentum and remains robust.

Performance of Regional Rural Banks (RRBs)

The government undertook various measures to optimise the resources and enhance the performance of the RRBs, says the Economic Survey 2025-26. These include measures such as their consolidation in four phases based on the principle of One-State-One-RRB. This reduced their number from 196 to 28 as of 1 May 2025.

Furthermore, the integration of the Core Banking Solution and other IT systems of the amalgamated RRBs into unified platforms has been undertaken.

Due to the such measures, their performance has improved significantly. In recent years, the financial health of the RRBs has improved. During FY24, they achieved a record consolidated net profit of ₹7.6 thousand crore, followed by a second-highest consolidated net profit of ₹6.8 thousand crore during FY25.

It is also noteworthy that RRBs have consistently exceeded the priority sector lending target of 75 per cent of their adjusted net bank credit over the years, underscoring their commitment to fulfilling their foundational objectives.

Major policy actions in the banking sector

The public sector banks (PSBs) have launched the credit assessment model (CAM) based on the digital footprints for MSMEs in 2025. The Economic Survey 2025-26 says that between 1st April and 30th November 2025, over ₹3.2 lakh crore MSME loan applications, amounting to more than ₹41.5 thousand crore, have been sanctioned by PSBs under the credit programmes of CAM.

This MSME model will leverage digitally fetched and verifiable data to enable automated loan appraisal for MSMEs, utilizing objective decisioning for all loan applications and model-based limit assessment for both existing-to-bank and new-to-bank MSME borrowers. Along with improving the ease of doing business for the MSMEs, this model also integrates the credit guarantee schemes, such as the Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE).

RBI has also initiated a significant reorganisation of its regulatory instructions, a move that signifies a transformative change in its regulatory communication.

Additionally, instructions issued by NABARD to RRBs, State Cooperative Banks, and Central Cooperative Banks were also consolidated in consultation with NABARD.

To strengthen the institutional mechanism for review of regulations, the RBI has constituted a regulatory review cell with a mandate to review every regulation in a comprehensive, objective, and systematic manner, at least once every 5-7 years. The cell has been operationalised effective from 1st October 2025.

Within the strengthened regulatory governance architecture, the RBI has also articulated principle-based guidance for the use of AI. It has introduced a Free AI framework for responsible AI, which is designed to foster financial innovation while ensuring robust risk management.

Microfinance and financial inclusion

With 95 per cent women borrowers and 80 per cent rural clientele, the Microfinance sector addresses segments where credit access has historically been limited.

The Economic Survey 2025-26 says that over the past decade, the microfinance sector has displayed steady growth, with active borrowers nearly doubling from 330 lakh in FY14 to 627 lakh in FY25. During this period, the gross loan portfolio of MFIs multiplied nearly seven times from ₹33,517 crore in FY14 to ₹2,38,198 crore in FY25. At the same time, MFI branch networks expanded from 11,687 branches to 37,380.

While the microfinance sector has evolved significantly over the past decade, its continued growth would hinge on strengthening enabling infrastructure (such as the tools to assess creditworthiness), ensuring responsible lending practices, and continuously strengthening institutional resilience to manage cyclical volatility.

Financial inclusion – trends and structural drivers

India has made significant strides in financial inclusion over the past decade. The government has introduced several targeted interventions. The Pradhan Mantri Jan Dhan Yojana (PMJDY), launched in 2014, has opened 55.02 crore accounts as of March 2025, with 36.63 crore in rural and semi-urban areas, establishing foundational savings and transaction infrastructure for previously unbanked populations. Building on this account base, credit-focused schemes have extended formal lending to underserved segments said the Economic Survey 2025-26.

The Stand-Up India Scheme offers bank loans ranging from ₹10 lakh to ₹1 crore to SC, ST, and women entrepreneurs for establishing greenfield enterprises. The PM Street Vendor's Atmanirbhar Nidhi (PM SVANidhi) scheme, launched in CY 2020, provides collateral-free working capital loans to street vendors. The Pradhan Mantri Mudra Yojana (PMMY), operational since April 2015, finances micro and small enterprises in manufacturing, trading, services, and allied agricultural activities.

These interventions have shown positive results. The number of adults possessing a bank account doubled between CY 2011 (35 per cent) and CY 2021 (89 per cent).

These structural shifts have been underpinned by two converging forces: regulatory innovation through India's digital infrastructure and government-led microfinance initiatives. Together, these drivers have expanded both the scale and depth of financial inclusion nationwide. Further the UPI has driven financial inclusion and become a flagship success story.

All the above efforts are reflected in the RBI’s Financial Inclusion (FI) Index, which measures the country's progress in achieving financial inclusion. The composite FI Index value rose to 67.0 in March 2025 from 64.2 in March 2024, with all sub-indices registering steady growth.

Performance of the Insolvency and Bankruptcy Code

The IBC established a unified framework for resolving corporate distress in India, replacing the earlier fragmented regime of multiple statutes with overlapping jurisdictions. Over nine years, IBC has contributed to improved credit discipline, a reduction in banking sector NPAs, and greater predictability in insolvency outcomes.

From the 1300 cases that resulted in a resolution process, creditors realised ₹3.99 lakh crore. Creditors recovered 94 per cent of the fair value of resolved businesses, and 170 per cent of what they would have received through liquidation. The data indicate that resolution, where feasible, delivers significantly

better outcomes for creditors than liquidation.

Reflecting these systemic improvements, S&P Global Ratings upgraded India's insolvency regime from 'Group C' to 'Group B' on 3 December 2025. The rating agency noted that average recovery rates have improved from 15-20 per cent under the pre-IBC regime to approximately 30 per cent, while resolution timelines have reduced from 6-8 years to about 2 years.

The Report has also acknowledged the role of judicial reinforcement of creditor rights, which have contributed to greater predictability and discipline in the resolution process.

****

NB/AD

(रिलीज़ आईडी: 2220002)

आगंतुक पटल : 3651