Ministry of Finance

CLEANER BALANCE SHEETS LEAD TO ENHANCED LENDING BY FINANCIAL INSTITUTIONS

GROWTH IN CREDIT OFFTAKE, INCREASED PRIVATE CAPEX TO USHER VIRTUOUS INVESTMENT CYCLE

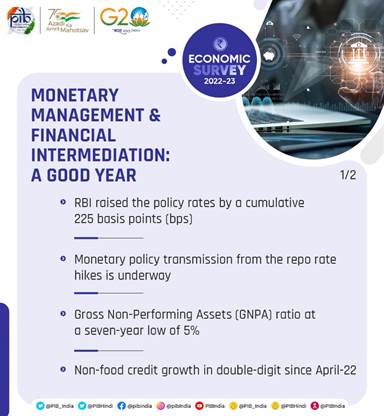

GROWTH OF NON-FOOD CREDIT OFFTAKE BY SCBs IN DOUBLE DIGIT SINCE APRIL 2022

GROSS NPA RATIO OF SCHEDULED COMMERCIAL BANKS (SCBs) AT 7-YEAR LOW

RECOVERY RATE FOR SCBs THROUGH IBC HIGHEST IN FY 22

प्रविष्टि तिथि:

31 JAN 2023 1:53PM by PIB Delhi

The balance sheet clean-up exercise over the last few years has enhanced the lending ability of financial institutions – seen in double-digit growth of non-food credit offtake by Scheduled Commercial Banks (SCBs) since April 2022. This was pointed out by the Economic Survey 2022-2023, tabled by the Union Minister for Finance & Corporate Affairs Smt. Nirmala Sitharaman in Parliament here today.

The Survey forecasts the financial system to play a key role in realizing objectives of Amrit Kaal - ushering a virtuous investment cycle backed by healthy balance sheet of banks, stronger capital base of NBFCs and robust growth in Assets under Management (AUM) of domestic mutual funds.

MONETARY DEVELOPMENTS

The Survey highlights that the return of inflation in 2022 across advanced and emerging economies led to a synchronous tightening of monetary policy.

RBI in its response initiated monetary tightening cycle in April 2022 and raised policy rates by a cumulative 225 basis points till December 2022 – leading to tightening of domestic financial conditions, reflected in lower growth of monetary aggregates. This was intended to support to economic growth while controlling inflation within target range.

LIQUIDITY CONDITIONS AND MONETARY POLICY TRANSMISSION

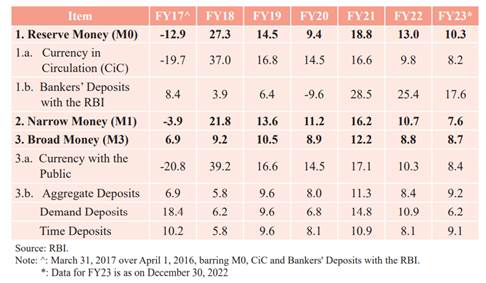

The Survey further adds that the “change in RBI’s policy stance in FY23 led to a moderation of surplus liquidity conditions that prevailed during the pandemic years.” The daily net liquidity absorption averaged ₹2.5 lakh crore during FY23 (up to 21 December 2022) as compared with ₹6.7 lakh crore in FY22.

Lending and deposit rates of banks increased during FY23 in consonance with the policy repo rate changes. Overall, the weighted average lending rate (WALR) on fresh and outstanding rupee loans rose by 135 bps and 71 bps, respectively, in FY23 (up to November 2022). On the deposit side, the weighted average domestic term deposit rate (WADTDR) on outstanding deposits increased by 59 bps in FY23 (up to November 2022). The increase in the WALRs on fresh loans was higher in the case of public sector banks, while that of the WADTDR on outstanding deposits and WALR on outstanding loans was higher for private banks.

G-SEC MARKET SCENARIO

In the Government securities (G-sec) market, the Survey notes that bond yields were on an upward trajectory until June 2022 on concerns of high inflation and policy rate hikes. These yields moderated in November and December 2022, aided by lower crude oil prices, a slower pace of rate hikes, and general moderation in global sovereign bond yields.

BANKING SECTOR

Economic Survey 2022-2023 points out that the efforts of RBI and the Government in terms of calibrated policy measures like strengthening the regulatory and supervisory framework, implementation of 4R’s approach of Recognition, Resolution, Recapitalization and Reforms have culminated in the enhancement of risk absorption capacity and a healthier banking system balance sheet both in terms of asset quantity and quality over the years.

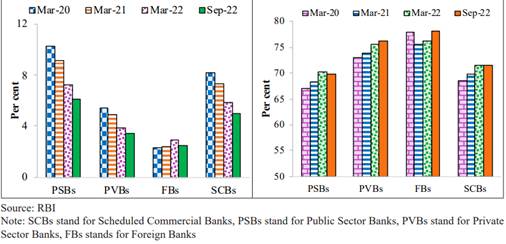

The Gross Non-Performing Assets ratio (GNPA) of SCBs has decreased from 8.2 per cent in March 2020 to a seven-year low of 5.0 per cent in September 2022. “Lower slippages and the reduction in outstanding GNPAs through recoveries, upgrades and write-offs led to this decrease”, the Survey said. As per the baseline scenario of the RBI’s stress testing framework, the declining tendency in the GNPA ratio is likely to continue and is projected to drop further to 4.9 per cent in March 2023. Moreover, with shrinking GNPAs, the Provisioning Coverage Ratio (PCR) has been increasing steadily since March 2021 and reached 71.6 per cent in September 2022.

CREDIT GROWTH

“The recovery in economic activity in FY22, along with the enhanced financial soundness of banks and corporates, has bolstered the expansion of non-food bank credit since June 2021. The YoY growth in non-food bank credit accelerated to 15.3 per cent in December 2022”, stated the Survey. Credit growth has been broad-based across sectors, with retail credit driving the growth primarily owing to rising demand for home loans.

Credit to agriculture and allied activities was supported by the Government’s concessional institutional credit and higher agricultural credit target. Industrial credit growth has been buoyed by a pick-up in credit to MSMEs, assisted by the Emergency Credit Line Guarantee Scheme (ECLGS) and the support of government’s production-linked incentive scheme and improvement in capacity utilization. Credit growth in services was driven by a recovery in credit to NBFCs, commercial real estate and trade sectors.

The Survey further adds that the well-capitalized banking system with a low NPA ratio and more robust corporate sector fundamentals will continue to enhance the flow of bank credit into productive investment opportunities, notwithstanding the rising interest rates.

CONTINUING RECOVERY OF NBFCs

Economic Survey 2022-2023 flags the consistent rise of NBFCs’ credit as a proportion to GDP as well as in relation to credit extended by SCBs. Supported by various policy initiatives, NBFCs could absorb the shocks of the pandemic. They built up financial soundness during FY22, marked by balance sheet consolidation, improvement in asset quality, augmented capital buffers and profitability.

The continuous improvement in asset quality is seen in the declining GNPA ratio of NBFCs from the peak of 7.2 per cent recorded during the second wave of the pandemic (June 2021) to 5.9 per cent in September 2022, reaching close to the pre-pandemic level.

Credit extended by NBFCs is picking up momentum, with the aggregate outstanding amount at ₹31.5 lakh crore as of September 2022. NBFCs continued to deploy the largest quantum of credit from their balance sheets to the industrial sector, followed by retail, services, and agriculture.

PROGRESS UNDER INSOLVENCY AND BANKRUPTCY CODE

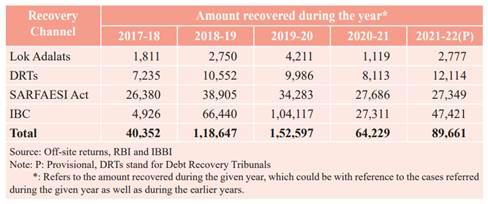

The Survey notes that in FY 2022, the total amount recovered by SCBs under IBC has been the highest compared to other channels such as Lok Adalats, SARFAESI Act and DRTs in this period.

Since the inception of the IBC in December 2016 it has augmented the Ease of Doing Business. 5,893 Corporate Insolvency Resolution Processes (CIRPs) had commenced by end-September 2022, of which 67 per cent have been closed. Sectoral analysis reveals that 52 per cent of the ongoing CIRPs belong to industry, followed by 37 per cent in the services sector by September 2022, observes the Survey.

As an evidence of behavioral change among Corporate Debtors (CDs), the Survey notes that until September 30 2022, 23,417 applications for initiation of Corporate Insolvency Resolution Proceedings (CIRP) of CDs having underlying default of ₹7.3 lakh crore were disposed of before their admission into CIRP, due to the fear of losing control over CD upon initiation of CIRP.

RM/PPG/PC

(रिलीज़ आईडी: 1894924)

आगंतुक पटल : 5144