Ministry of Finance

India’s Sovereign Credit Ratings do not capture its Fundamentals: Economic Survey

Rating Methodology needs to be made more transparent and objective, To Reflect Willingness and Ability of Country to meet Sovereign Obligations: Survey

Survey Calls for Fiscal Policy to focus on growth, not withstanding Credit Ratings

प्रविष्टि तिथि:

29 JAN 2021 3:37PM by PIB Delhi

The Economic Survey has called for sovereign credit ratings methodology to be made more transparent, less subjective and better attuned to reflect an economy’s fundamentals. The Union Minister for Finance & Corporate Affairs, Smt. Nirmala Sitharaman tabled the Economic Survey 2020-21 in Parliament today.

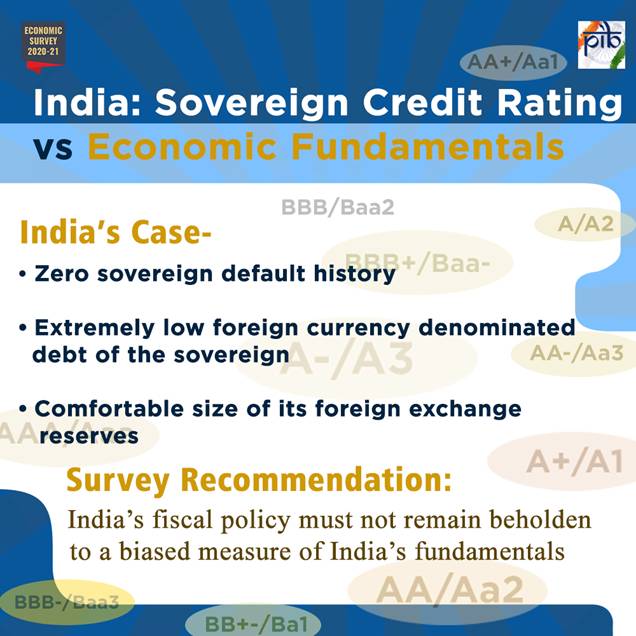

The Survey notes that never in the history of sovereign credit ratings, has the fifth largest economy in the world been rated at the lowest rung of the investment grade (BBB-/Baa3) except in the case of China and India. Reflecting on the economic size and thereby ability to repay debt, at all other times, the fifth largest economy has been predominantly rated AAA.

Further, it points out that India’s sovereign credit ratings do not reflect its fundamentals. Within its sovereign credit ratings cohort, India is a clear outlier on several parameters, i.e. it is rated significantly lower than mandated by the effect on the sovereign rating of the parameter. These include GDP growth rate, inflation, general government debt (as per cent of GDP), current account balance (as per cent of GDP), cyclically adjusted primary balance (as per cent of potential GDP), short-term external debt (as per cent of reserves), reserve adequacy ratio political stability, rule of law, control of corruption, investor protection, ease of doing business, and sovereign default history. This outlier status remains true not only for the current period but also during the last two decades.

Effect of Sovereign Credit Rating Changes

As ratings do not capture India’s fundamentals, the Survey highlighted that past episodes of sovereign credit rating changes have not had major adverse impact on select indicators such as Sensex return, foreign exchange rate and yield on government securities. The same have no or weak correlation with macroeconomic indicators, it indicated.

However, the Survey points out that the Sovereign Credit Ratings can be pro-cyclical and affect equity and debt FPI flows of developing countries, causing damage and worsening crisis. Hence, it has called for all developing countries to come together to address the bias and subjectivity inherent in sovereign credit ratings methodology and bring in more transparency. India has already raised the issue of pro-cyclicality of credit ratings in G20.

Sovereign Credit Rating Needs to Reflect Willingness and Ability to Pay

Credit ratings map the probability of default and therefore reflect the willingness and ability of borrower to meet its obligations. The Survey observes that India’s willingness to pay is unquestionably demonstrated through its zero sovereign default history.

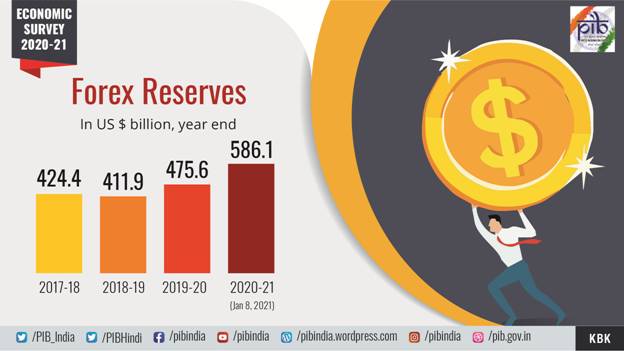

India’s ability to pay can be gauged not only by the extremely low foreign currency-denominated debt of the sovereign but also by the comfortable size of its foreign exchange reserves that can pay for the short term debt of the private sector as well as the entire stock of India’s sovereign and non-sovereign external debt. India’s sovereign external debt as per cent of GDP stood at a mere four per cent as of September 2020.

The Survey describes that India’s forex reserves can cover an additional 2.8 standard deviation negative event, i.e. an event that can be expected to manifest with a probability of less than 0.1 per cent, after meeting all short-term debt. Further, India’s forex reserves stood at US$ 584.24 billion as of January 15, 2021, greater than India’s total external debt (including that of the private sector) of US$ 556.2 billion as of September 2020. Given private export earnings, India’s large forex reserves are in fact an under-estimation of its ability to repay its short-term obligations. In corporate finance parlance, India resembles a firm that has negative debt, whose probability of default is zero by definition.

The Survey evidences instances of systemic under-assessment and bias in the sovereign credit ratings over a period of at least two decades. The findings are consistent with a large academic literature that highlights bias and subjectivity in sovereign credit ratings, especially against countries with lower ratings and developing economies, it says.

For the above reasons, the Economic Survey advises that India’s fiscal policy should not be restrained by biased and subjective ratings; rather it should focus on growth and development, reflecting Gurudev Rabindranath Tagore’s sentiment of a mind without fear.

***

RM/AUK

(रिलीज़ आईडी: 1693201)

आगंतुक पटल : 2795