PIB Backgrounder

Kisan Credit Card: Fueling Growth in Agriculture

Strengthening Farmers’ access to capital

प्रविष्टि तिथि:

11 MAR 2026 11:47AM by PIB Delhi

|

Text Box: Key Takeaways

- The Kisan Credit Card (KCC) provides timely, affordable, and collateral-free credit to farmers, including small, marginal, tenant farmers and SHGs/JLGs.

- Under the Modified Interest Subvention Scheme (MISS), the loan limit has been enhanced to Rs. 5 lakh, with collateral-free credit raised to Rs. 2 lakh per borrower.

- Over 7.72 crore KCCs are active nationwide, with outstanding loans of about Rs. 10.2 lakh crore.

- The KCC platform has onboarded 457 banks and received more than 1,998.7 lakh applications across commercial, regional, rural, and cooperative banks

|

Introduction

The agriculture and allied activities sector have historically formed the backbone of the Indian economy, making substantial contributions to national income, employment generation, and rural livelihoods. With nearly 46.1 per cent of the population dependent on agriculture and allied activities for their sustenance, ensuring financial security and improved access to institutional credit for farmers remains a central policy priority for the Government. In this context, a set of targeted interventions has been introduced to strengthen agricultural finance, with particular emphasis on expanding and modernizing the Kisan Credit Card (KCC).The Revised Kisan Credit Card (2020) scheme seeks to ensure that farmers have access to adequate and timely credit for a wide range of agricultural requirements, including short-term crop cultivation, post-harvest operations, marketing-related expenses, household consumption needs, working capital for farm maintenance, and investment credit for allied and non-farm activities.

Evolution of Kisan Credit Card and its Features

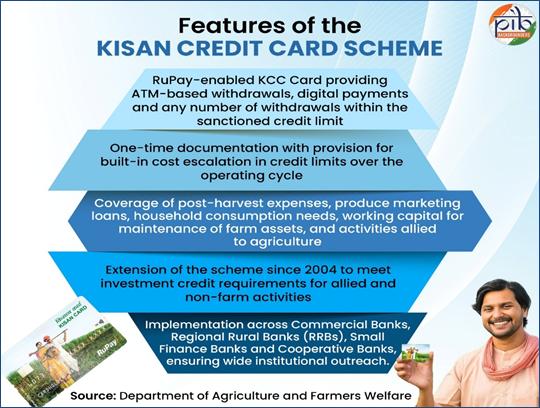

The Kisan Credit Card (KCC) Scheme, introduced in 1998, was designed to simplify and expedite farmers’ access to short-term institutional credit for crop production. It provides working capital and investment credit for allied activities and covers post-harvest and marketing expenses, thereby offering comprehensive financial support to enhance farm incomes. To further improve the affordability of credit under the KCC, the Government launched the Modified Interest Subvention Scheme (MISS) as a Central Sector Scheme in 2006–07. The scheme ensures farmers have access to credit at affordable rates through the Kisan Credit Card (KCC). The scheme also supports farmers in recovering from natural calamities and promotes timely loan repayment, thereby easing overall financial stress. Over time, it expanded to cover allied and non-farm activities, with the Revised KCC Scheme (2020) providing integrated, single-window credit support.

The revised KCC offers a RuPay-enabled card with flexible withdrawals, digital payments, and one-time documentation, making access to credit simple and efficient. It covers cultivation, post-harvest needs, allied, and non-farm activities, and is implemented through commercial, regional rural, and cooperative banks to ensure broad outreach.

Eligible Beneficiaries of the Kisan Credit Card

The Kisan Credit Card (KCC) Scheme covers a wide range of farmer categories to promote inclusive and equitable access to institutional credit. It extends coverage to:

- individual farmers and joint borrowers who are owner-cultivators,

- tenant farmers, oral lessees, and sharecroppers.

- In addition, the scheme also includes Self Help Groups (SHGs) and Joint Liability Groups (JLGs), including groups formed by tenant farmers and sharecroppers,

thereby ensuring broader financial inclusion across diverse farming communities.

Onboarding of Farmers through the KCC application

To streamline farmer onboarding and improve access to institutional credit, facilitative measures have been implemented under the Kisan Credit Card.

- A simplified one-page KCC application form has been introduced, with basic applicant details pre-filled from banks’ PM-KISAN records, and farmers are required to submit copies of land records and information on the crops cultivated.

- The form is widely disseminated through national newspaper advertisements and made available for download on the websites of all Scheduled Commercial Banks (SCBs), the Department of Agriculture and Farmers Welfare (agricoop.gov.in), and the PM-KISAN portal (pmkisan.gov.in).

- Common Service Centres (CSCs) have been authorized to assist in completing and digitally transmitting applications to the concerned bank branches, thereby expanding outreach.

Kisan Rin Portal: Digital transformation of KCC implementation

To strengthen the implementation and monitoring of the Kisan Credit Card (KCC) scheme, the Government launched the Kisan Rin Portal (KRP) in September 2023 as a unified digital platform that integrates:

- farmer profiles,

- loan disbursement data,

- interest subvention claims, and

- scheme performance metrics.

For farmers, the portal simplifies access to low-cost institutional credit, expands coverage to allied activities such as dairy, poultry, fisheries, and beekeeping, and enables faster loan processing through seamless digital integration with banks and cooperative institutions.

For banks and lending agencies, KRP facilitates the automated submission and processing of Interest Subvention (IS) and Prompt Repayment Incentive (PRI) claims, reduces delays through end-to-end digitization, and enhances transparency and accountability in claim verification and settlement. Overall, the portal has significantly improved operational efficiency, monitoring, and transparency in agricultural credit administration.

Enhancing Farmers’ Access to Affordable Credit under MISS and KCC

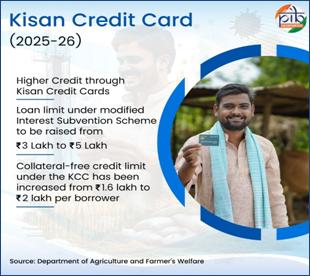

In 2025–26, the Government of India enhanced the Kisan Credit Card (KCC) lending limit, which includes:

- the crop loan limit under MISS, which has been raised from Rs 3 lakh to Rs 5 lakh.

the credit limit for fisheries and allied activities has been increased from Rs 2 lakh to Rs 5 lakh

- the collateral-free credit limit has increased from Rs 1.6 lakh to Rs 2 lakh per borrower, effective from 1 January 2025.

- Short-term agri-loans up to Rs 3 lakh are available at 7% interest, with an additional 3% subvention for timely repayment, reducing the effective rate to 4%.

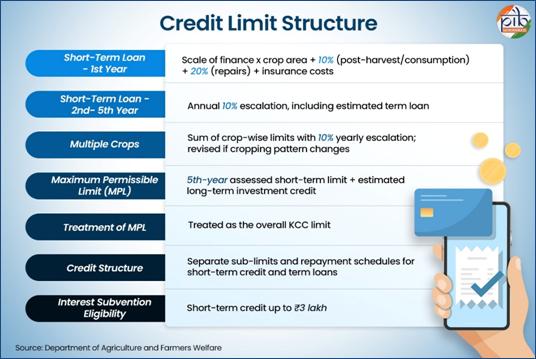

Credit Limit and Loan provisions under KCC

Under the Kisan Credit Card (KCC), term loans and composite credit limits are structured differently for marginal and non-marginal farmers, taking into account their landholding size, investment capacity, and livelihood requirements. While non-marginal farmers are provided asset-linked term loans for long-term agricultural and allied investments, marginal farmers are provided with flexible, need-based credit limits that integrate short-term production credit, consumption needs, and minor investment requirements within a single composite Kisan Credit Card limit.

Provisions for all farmers other than marginal farmers

Provisions for Marginal Farmers

A flexible limit of Rs 10,000 to Rs 50,000 may be sanctioned based on factors such as landholding size and cropping patterns. The composite KCC limit is to be fixed for a period of five years. In cases where higher credit is required due to changes in cropping patterns or scale of finance, the limit may be revised in accordance with prescribed estimation norms. This limit is designed to cover:

- post-harvest and warehouse-related credit requirements,

- routine farm and consumption expenses, and

- short-term investments, including the purchase of farm equipment or the establishment of an allied enterprise, as assessed by the branch manager and independent of land valuation.

Scale and Financial Outreach of the KCC

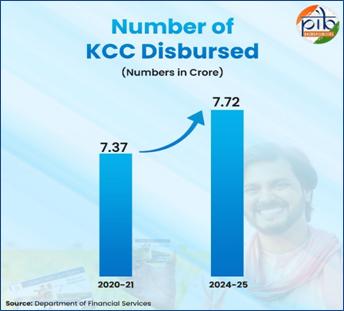

More than 7.72 crore Kisan Credit Cards (KCCs) are currently operational across the country, with an outstanding credit amounting to Rs. 10.2 lakh crore. This reflects the extensive reach of the KCC scheme in facilitating access to institutional credit for farmers and underscores its critical role in supporting agricultural and allied activities through affordable, timely financing.

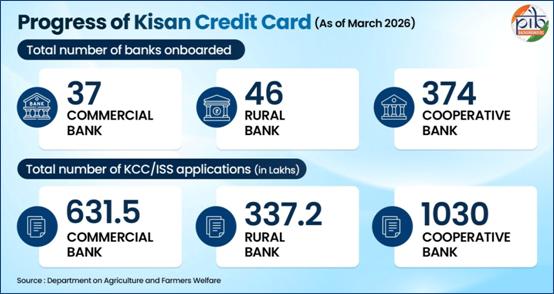

Under the Kisan Credit Card (KCC) platform, a total of 457 banks has been onboarded, including 37 commercial banks,46 regional rural banks, and 374 cooperative banks. It indicates a diversified delivery architecture to ensure broad geographic coverage and inclusive access to institutional credit for farmers nationwide. Across these institutions, a total of 1,998.7 lakh kisan credit card applications have been processed, of which 631.5 lakh were through commercial banks, 337.2 lakh through regional rural banks, and 1030.0 lakh through cooperative banks. It reflects the broad institutional participation in the KCC implementation and highlights the central role of cooperative banks in extending agricultural credit, particularly at the grassroots level.

In 2018–19, the Government of India extended the Kisan Credit Card (KCC) facility to fishers and fish farmers to meet their working capital requirements, thereby enabling timely access to institutional credit for fisheries and aquaculture activities. The total KCC issuance peaked, reflecting the scheme's expanding reach to support diverse agricultural activities.

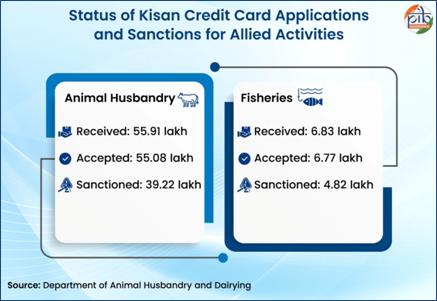

The facts and figures indicate a strong institutional response to credit demand in allied agricultural activities. In animal husbandry, the exceptionally high acceptance rate, 55.08 lakh out of 55.9 lakh applications, reflects broad eligibility, effective screening mechanisms, and sustained policy support for the sector. The sanctioning of 39.22 lakh applications further suggests substantial credit flow, translating into actual financial support.

Similarly, in fisheries, 6.83 lakh applications were received, of which 6.77 lakh were accepted. The sanctioning of 4.82 lakh applications indicates meaningful conversion of demand into credit access. Overall, these outcomes underscore the growing integration of allied sectors into formal credit systems.

Advancing Affordable Credit and Farm Productivity

By easing access to working capital, the Kisan Credit Card (KCC) scheme is facilitating timely investment in quality agricultural inputs, thereby contributing to enhanced farm productivity and higher incomes.

- Affordable Institutional Credit: The scheme continues to offer institutional credit at a highly concessional interest rate of 4%. This makes it one of the most affordable agricultural credit instruments globally, ensuring easier access for small and marginal farmers.

- Flexible Credit facilities: The KCC continues to provide revolving credit facilities with a validity of up to 5 years, allowing farmers to withdraw funds as needed for their production.

- Risk Mitigation Support: To mitigate risks arising from natural calamities, interest is not charged for up to 1 year, extendable to 5 years in cases of severe disasters.

- Collateral-Free Loans: Enabling farmers to avail loans up to Rs. 2 Lakh without collateral, significantly reducing entry barriers to formal credit.

- Empowering small and marginal farmers: With approximately 76 percent of agricultural credit accounts held by these farmers, the scheme plays a critical role in empowering the most vulnerable segments of the farming community.

- Boost in Farming Productivity: Enabling farmers to invest in improved seeds, fertilizers, and farm equipment, leading to better yields, enhanced incomes, and strengthened agricultural resilience.

Government Initiatives to Enhance Accessibility of the KCC

The Government has undertaken a series of measures to enhance the accessibility, coverage, and effectiveness of the Kisan Credit Card (KCC) Scheme.

- To improve awareness, the Union and State Governments, in collaboration with the Reserve Bank of India, NABARD, and banking institutions, have implemented extensive Information, Education, and Communication (IEC) campaigns and farmer outreach programmes.

- Under the Atmanirbhar Bharat Abhiyan, a nationwide KCC Saturation Drive is being conducted to ensure coverage of all eligible farmers, including those engaged in animal husbandry, dairy, and fisheries, through district-level weekly camps.

- In addition, the RuPay KCC has facilitated convenient access to short-term agricultural credit and promoted digital transactions. It has also reduced reliance on cash and informal lending sources, thereby enabling farmers to avail interest subvention benefits.

Collectively, these government initiatives have strengthened financial inclusion and improved the delivery of institutional credit by enabling a secure, interoperable payment framework.

Conclusion

Access to affordable and timely institutional credit is central to sustaining agricultural livelihoods and strengthening rural economies. The Kisan Credit Card (KCC) Scheme has addressed this need by creating a reliable credit mechanism that supports cultivation, allied activities, and post-harvest requirements within a single, flexible framework. The progressive evolution of the scheme reflects a shift from transaction-based lending towards a more holistic approach that aligns credit availability with farmers’ production cycles and income flows.

Recent reforms, including enhanced credit limits, expanded coverage to allied sectors, and digital integration through the Kisan Rin Portal, have significantly improved outreach, transparency, and governance. By enabling data-driven monitoring, expediting loan processing, and ensuring transparent claim settlement, these measures have strengthened the operational efficiency of agricultural credit delivery. In the context of increasing climate-related and market risks, the KCC scheme serves as a critical policy instrument to enhance financial resilience, promote the formalization of credit, and support sustainable agricultural growth, thereby contributing to inclusive rural development and long-term sectoral stability. Its continued strengthening will remain essential for advancing inclusive rural development and long-term agrarian stability.

References

Department of Agriculture and Farmers Welfare

https://www.pib.gov.in/PressReleasePage.aspx?PRID=2099696

https://fasalrin.gov.in/

https://www.pib.gov.in/PressReleasePage.aspx?PRID=2132139

https://www.pib.gov.in/PressReleseDetailm.aspx?PRID=1958531&utm

https://www.pib.gov.in/FactsheetDetails.aspx?Id=148600

https://financialservices.gov.in/beta/sites/default/files/DFS-Data-Snapshot.pdf

Lok Sabha and Rajya Sabha Questions

https://sansad.in/getFile/loksabhaquestions/annex/185/AU4180_nfJzOf.pdf?source=pqals

https://sansad.in/getFile/loksabhaquestions/annex/185/AU1365_spXbvr.pdf?source=pqals

https://sansad.in/getFile/loksabhaquestions/annex/185/AU2500_MY7k37.pdf?source=pqals

https://sansad.in/getFile/loksabhaquestions/annex/185/AU1588_urrFbf.pdf?source=pqals

https://sansad.in/getFile/annex/267/AS338_apRnsi.pdf?source=pqars

RBI

https://www.rbi.org.in/commonman/english/scripts/Notification.aspx?Id=2311&utm

https://rbidocs.rbi.org.in/rdocs/content/pdfs/10MCKCC040718_AN.pdf

Economic Survey

https://www.indiabudget.gov.in/economicsurvey/doc/eschapter/echap09.pdf

https://www.indiabudget.gov.in/doc/budget_speech.pdf

See in PDF

***

PIB Research

(रिलीज़ आईडी: 2238004)

आगंतुक पटल : 8322