Ministry of Finance

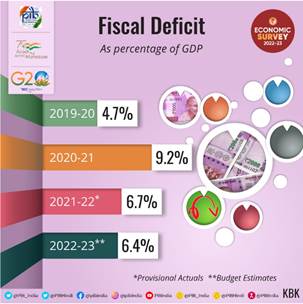

GOVERNMENT ON TRACK TO ACHIEVE FISCAL DEFICIT TARGET OF 6.4%

15.5% YoY GROWTH IN GROSS TAX REVENUE FROM APRIL TO NOVEMBER 2022

Rs. 13.40 LAKH CRORE COLLECTED AS GST REVENUE IN FIRST 3 QUARTERS OF FY23

NUMBER OF GST TAX PAYERS DOUBLED TO 1.4 CRORE FROM 70 LAKH

24.8 % YoY GROWTH IN GROSS GST COLLECTIONS DURING APRIL- DECEMBER 2022

DIRECT TAXES REGISTER A GROWTH OF 26% YoY DURING APRIL- NOVEMBER 2022

CAPITAL EXPENDITURE TO RISE BY 2.9% IN FY23 OVER LONG TERM AVERAGE OF 1.7% OF GDP

GOVERNMENT DEBT DECLINES FROM 59.2% OF GDP IN FY21 TO 56.7% IN FY22

GENERAL GOVERNMENT DEBT TO GDP RATIO INCREASED BY A MODEST 3% SINCE 2005 AS COMPARED TO SUBSTANTIAL INCREASE IN MOST COUNTRIES

प्रविष्टि तिथि:

31 JAN 2023 1:49PM by PIB Delhi

“The gradual decline in the Union government's fiscal deficit as a % of GDP, in line with the fiscal glide path envisioned by the government, is a result of careful fiscal management supported by buoyant revenue collection over the last two years” stated the Economic survey 2022-23 tabled by the Union Minister for Finance and Corporate Affairs Smt. Nirmala Sitharaman today in Parliament.

According to the Survey, fiscal deficit is expected to be at 6.4% of GDP in FY 23. The Survey highlighted that conservative budget assumptions provided a buffer during global uncertainties. The resilience in the fiscal performance was due to a recovery in economic activity and buoyancy in revenues.

Gross Tax Revenue

Gross Tax Revenue registered a Year on year (YoY) growth of 15.5 % from April to November 2022, and the Net Tax Revenue to the Centre after the assignment to states grew by 7.9 % on a YoY basis, stated the Survey. Structural reforms like the introduction of GST and the digitalisation of economic transactions have led to the greater formalisation of the economy and hence expanded the tax net and enhanced tax compliance. Thus revenues have grown at a pace much higher than the growth in GDP.

The Economic Survey highlighted that Direct taxes grew at 26 % Year On Year basis due to corporate and personal income tax growth in FY22. The Survey further added that growth rates observed in the major direct taxes during the first eight months of FY23 were much higher than their corresponding longer-term averages.

The Survey informed that high imports have led to a 12.4 % YoY growth in the customs collection from April to November 2022. The excise duty collection has declined by 20.9 % from April to November 2022 on a YoY basis.

Buoyant GST Collection

“The GST Tax payers doubled to 1.4 crore from 70 lakhs in 2022. The gross GST collections were ₹13.40 lakh crore from April to December 2022. Thus, implying a YoY growth of 24.8 % with an average monthly collection of ₹1.5 lakh crore”, noted the Survey. It further highlighted that improvement in GST collections has been due to the nationwide drive against GST evaders and fake bills and systemic changes introduced such as rate rationalisation correcting inverted duty structure.

Disinvestment

“Out of the budgeted amount of ₹65,000 crore for FY23, 48 % has been collected as of 18 January 2023 as the pandemic-induced uncertainty, the geopolitical conflict, and the associated risks have posed challenges before the plans and prospects of the government's disinvestment targets over the last three years” stated the Economic Survey 2022-23.

The Survey added that government has reaffirmed its commitment towards privatisation and strategic disinvestment of Public Sector Enterprises by implementing the New Public Sector Enterprise Policy and Asset Monetisation Strategy.

Capital expenditure

According to the Survey, the capital expenditure by the Central Government has steadily increased from a long-term average 2.5% of GDP in FY22 PA. It is further budgeted to increase to 2.9% of GDP in FY23 highlighting an improvement in the quality of Government expenditure over the years.

The Survey informed that ₹7.5 lakh crore of Capital Expenditure is budgeted for FY23, of which more than 59.6 % has been spent from April to November 2022. During this period, capital expenditure registered a YoY growth of over 60 %, much higher than the long-term average growth of 13.5 % recorded in the corresponding period from FY16 to FY20. Rs.1.5 lakh core were allocated to road transport and highways, Rs.1.20 lakh crore to railways, 0.7 lakh crore to defence and 0.3 lakh crore to telecommunications in FY22. It is considered as a counter-cyclical fiscal tool strengthening aggregate demand, generates employment and boosts other sectors.

To push for enhancing Capex from all directions, the Centre announced several incentives to boost states' capital expenditure in the form of long-term interest-free loans and capex-linked additional borrowing provisions

Revenue Expenditure

The revenue expenditure of the Union government was brought down from 15.6% of GDP in FY21 to 13.5% of GDP in FY22 Provisional Actual (PA). This contraction was led by a reduction of the subsidy expenditure which was brought down from 3.6% of GDP in FY21 to 1.9% of GDP in FY22 PA. It was further budgeted to reduce to 1.2% of GDP in FY23. However, around 94.7% of the budgeted expenditure on subsidies has been utilised from April to November 2022 due to the sudden outbreak of geopolitical conflict resulting in higher international prices for food, fertiliser and fuel. Thus, the revenue expenditure from April to November 2022 has grown by over 10% on a YoY basis, higher than the growth noted in the corresponding period last year.

Interest payments as a proportion of receipts went up after the pandemic outbreak. However, in the medium term, as we move along the fiscal glide path, buoyancy in revenues, aggressive asset monetisation, efficiency gains, and privatisation would help pay down the public debt, thus bringing down interest payments and releasing more monies for other priorities, highlights the Economic Survey.

Overview of State Government Finances

The combined Gross Fiscal Deficit (GFD) of the States, which increased to 4.1% of GDP in FY21, was brought down to 2.8% in FY22 PA. Given the geopolitical uncertainties, the consolidated GFD-GDP ratio for States has been budgeted at 3.4% in FY23. However, from April- November 2022, the combined borrowings of the 27 major states have just reached 33.5% of their total budgeted borrowings for the year. The data from last three years shows that states had unutilised borrowing limits.

The capital outlay of States grew by 31.7% in FY22 PA. This increase is attributable to strong revenue buoyancy and the support provided by the Centre in terms of advance releases of payments to the states, GST compensation payments, and interest-free loans.

Transfer from Centre to States

Total transfers to States comprising the share of States in Union taxes devolved to the States, Finance Commission Grants, Centrally Sponsored Schemes (CSS), and other transfers, have risen between FY19 and FY23 BE. The Finance Commission had recommended allocation of ₹1.92 lakh crore for FY23.

GST Compensation payments during crisis

To meet the shortfall in GST compensation for States, the Government, in addition to the release of regular GST compensation from the Fund, borrowed Rs. 2.69 lakh crore during FY21 and FY22 and passed it on to States. Moreover, the cess payments and tax devolution instalments to the States were frontloaded to give them early access to funds. Even though the total Cess collection until November 2022 was insufficient to make the entire payment to the States, the Centre released the balance from its resources.

Enhanced borrowing limits for states and incentives for reforms

Since the pandemic outbreak, the Centre has kept the Net Borrowing Ceiling of the State Governments above the Fiscal Responsibility Legislation (FRL) threshold. It was fixed at 5 % of GSDP in FY21, 4 % of GSDP in FY22 and 3.5 % of GSDP in FY23, a part of which was linked to reforms such as implementing the 'One Nation One Ration Card' System, ease of doing business reform, urban Local body/ utility reforms, and power sector reforms etc. The survey observes the progress made by various states in these reforms.

Centre’s support towards States’ capital expenditure

Amounts of Rs. 11,830 crore and Rs. 14,186 crore were provided to states in FY21 and FY22 as 50-year interest-free loans to state governments under the 'Scheme for Special Assistance to States for Capital Investment'. During the year FY23, the allocation under the Scheme has been raised to ₹1.05 lakh crore to give further impetus to State Capex plans.

Debt Profile of the Government

IMF projects the global government debt at 91% of GDP in 2022, about 7.5% points above the pre-pandemic levels. In this global backdrop, the total liabilities of the Union Government moderated from 59.2% of GDP in FY21 to 56.7% in FY22 (P).

India's public debt profile is relatively stable and is characterised by low currency and interest rate risks. Of the Union Government's total net liabilities in end-March 2021, 95.1% were denominated in domestic currency, while sovereign external debt constituted 4.9%, implying low currency risk. Further, sovereign external debt is entirely from official sources, which insulates it from volatility in the international capital markets, highlights the Economic Survey.

Furthermore, Public debt in India is primarily contracted at fixed interest rates, with floating internal debt constituting only 1.7% of GDP in end-March 2021. The debt portfolio is, therefore, insulated from interest rate volatility.

Consolidating General Government Finances

The General Government liabilities as a proportion of GDP increased steeply during FY21 on account of the additional borrowings made by Centre and States on account of the pandemic. However, the ratio has come off its peak in FY22 (RE), as observed by the Economic Survey. The General Government deficits as a percentage of GDP have also consolidated after their peak in F21.

A positive growth-interest rate differential

The Survey notes that the emphasis on capex in recent years is expected to boost GDP growth directly, and indirectly through multiplier effects on private consumption expenditure and private investment. Higher GDP growth would thereby facilitate buoyant revenue collection in the medium term, enabling a sustainable fiscal path. The General Government Debt to GDP ratio increased from 75.7% of end-March 2020 to 89.6% at the end of the pandemic year FY21. It is estimated to decline to 84.5% of GDP by end-March 2022. The emphasis on capex-led growth will enable India to keep the growth-interest rate differential positive. A positive growth-interest rate differential keeps the debt levels sustainable.

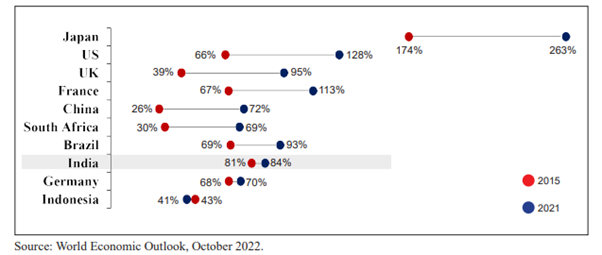

The change in General Government debt to GDP ratio from 2005 to 2021 has been substantial across the countries. For India, this increase is modest, from 81% of GDP in 2005 to around 84% of GDP in 2021. It has been possible on the back of resilient economic growth during the last 15 years leading to a positive growth-interest rate differential, which, in turn, has resulted in sustainable Government debt to GDP levels, explains the Economic Survey.

Fig.- Comparison of General Government debt to GDP ratio in 2005 with 2021 across the countries

******

RM/PPG/MK/PM

(रिलीज़ आईडी: 1894921)

आगंतुक पटल : 11416