Others

Indian Tea Sector: Production, Trade, Welfare and Sustainability

Posted On:

05 MAY 2026 6:29PM

Kolkata, 05 May, 2026

Institutional Profile and Mandate

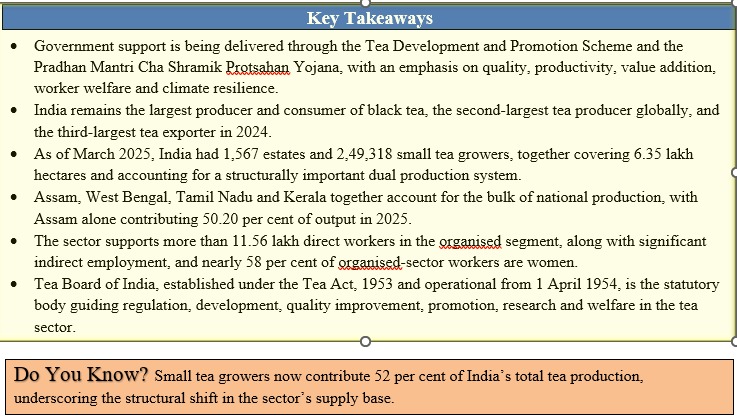

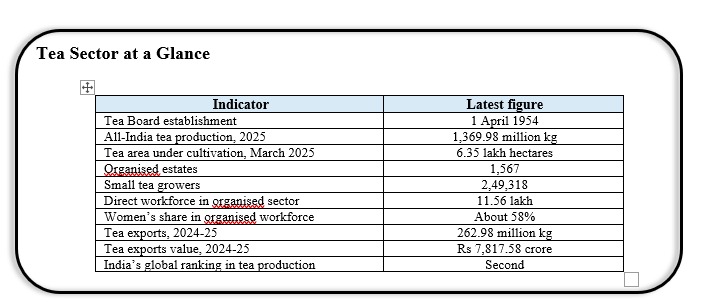

The Tea Board of India is the statutory authority responsible for guiding the development of the Indian tea industry. It was established on 1 April 1954 under the Tea Act, 1953, and functions under the administrative control of the Department of Commerce, Ministry of Commerce and Industry, Government of India. Its mandate is broad: the Board is expected not only to regulate and promote the tea economy, but also to support scientific research, strengthen market structures, protect quality standards, improve labour welfare and sustain long-term competitiveness.

The Board’s core functions include regulating production and the extent of tea cultivation, improving tea quality, encouraging cooperative effort among growers and manufacturers, supporting research and demonstration farms, training tea tasters and fixing tea grades, promoting domestic consumption, registering and licensing manufacturers, brokers and blenders, improving marketing, collecting and disseminating sector statistics, and helping to secure better working conditions for tea workers. In practice, this means that the Board operates at the intersection of agriculture, trade, labour welfare, research and branding.

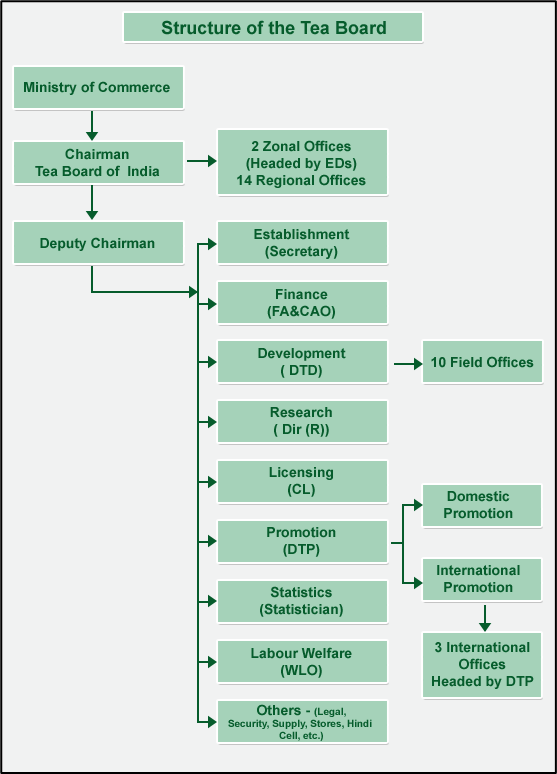

The organisation is structured around specialised divisions. Development focuses on the Tea Development and Promotion Scheme; Promotion handles domestic and export promotion; Finance manages the Board’s financial systems and internal audit; licensing performs regulatory functions under the applicable control orders; Research coordinates with tea research institutes and the Board’s own research centre at Darjeeling; Statistics collects and disseminates sector data; Establishment manages general administration and human resources; Law handles legal matters; and Raj Bhasha oversees Hindi-related official work. The leadership of the Board is currently headed by Shri Nitin Kumar Yadav, IAS, as Chairman, while Shri C. Murugan, IAS, serves as Deputy Chairperson and Chief Executive Officer.

This institutional design matters because tea is not merely a crop. It is a long-duration plantation commodity, a labour-intensive livelihood system, a traded beverage with strong branding value and a product whose quality is shaped by both agronomy and processing. The Tea Board’s mandate therefore extends across the entire value chain, from green leaf to finished tea and from rural field practices to global market access.

|

Do You Know? Tea Board’s annual reports and accounts are laid before both Houses of Parliament and subsequently published on its website, making the institution one of the most visible statutory bodies in the plantation sector.

|

Indian Tea Sector Overview

India’s tea industry is both geographically diverse and economically significant. Tea is grown in 15 States. Assam, West Bengal, Tamil Nadu and Kerala are the principal producing states, while Tripura, Himachal Pradesh, Uttarakhand, Bihar and Karnataka are established but smaller contributors. A newer belt of non-traditional States, including Arunachal Pradesh, Manipur, Meghalaya, Mizoram, Nagaland and Sikkim, has also entered the tea map of India. The country’s tea landscape therefore combines old plantation economies with newer small-grower clusters and diverse agro-climatic conditions.

The country’s tea identity is also strongly regional. Darjeeling, Assam, Nilgiri and Kangra teas are widely recognised for their distinctive sensory and market attributes. Darjeeling tea is celebrated for its aroma and muscatel character and enjoys GI protection. Assam tea is known for its full-bodied, strong and malty cup profile and is the single largest contiguous tea-growing region in the world. Nilgiri tea is valued for its floral aroma and clarity of liquor, while Kangra tea is known for its rich aroma and distinct flavour. Sikkim tea has developed a niche as a fully organic tea. Dooars-Terai teas are appreciated for their heavy, full-bodied liquor, and Tripura has also emerged as an important CTC-producing state.

India is the largest producer and consumer of black tea in the world. It is the second-largest tea producer overall and, in 2024, stood as the third-largest tea exporter globally. Tea remains deeply embedded in domestic consumption patterns, but it is also a major export crop and a source of foreign exchange. The sector’s importance is amplified by its labour intensity and its concentration in rural and remote regions, where plantation activity supports households, local trade and allied services.

The supply structure of the industry has evolved over time. The organised segment, represented by tea estates, continues to play a major role, but small tea growers have become a dominant force in raw leaf production. As of March 2025, 1,567 estates and 2,49,318 small tea growers together covered 6,35,364.61 hectares. Estates accounted for 4,21,460.70 hectares, while small tea growers accounted for 2,13,903.91 hectares. This dual structure has important implications for quality control, marketing, mechanisation, farmer organisation and price transmission.

The figures above reflect the scale and reach of the sector, but they also point to the policy complexity of governing a commodity that is simultaneously an agricultural product, an export brand and a rural livelihood base.

Production Trends, Regional Concentration and Market Structure

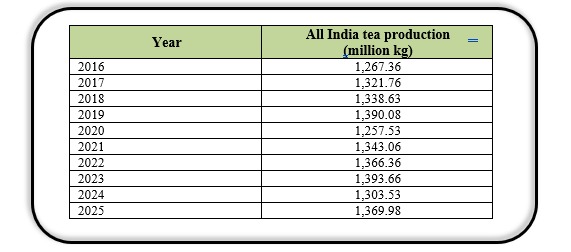

India’s tea production has shown resilience over the last decade, though it has also been affected by weather shocks, pest pressure, ageing bushes and labour constraints. All-India production stood at 1,267.36 million kg in 2016, rose gradually to 1,390.08 million kg in 2019, dipped during the pandemic year to 1,257.53 million kg in 2020, and recovered thereafter. Output reached 1,393.66 million kg in 2023, moderated to 1,303.53 million kg in 2024 and rose again to 1,369.98 million kg in 2025. The trajectory shows an industry capable of recovery, but also one that remains highly exposed to climatic and structural variability.

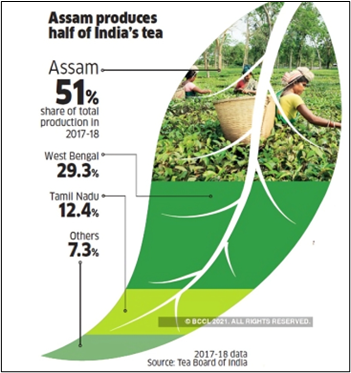

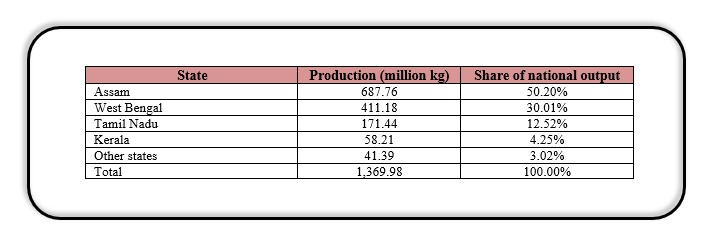

Production remains sharply concentrated in a few states. In 2025, Assam contributed 687.76 million kg, or 50.20 per cent of national production. West Bengal produced 411.18 million kg, accounting for 30.01 per cent. Tamil Nadu contributed 171.44 million kg, while Kerala produced 58.21 million kg. The balance came from other States. This concentration explains why state-specific climatic and logistical conditions have such a strong impact on national output and price dynamics.

CTC tea dominates domestic consumption, while orthodox tea, green tea and specialty teas occupy smaller but strategically important niches, particularly in export markets. India also produces oolong, white tea and other speciality varieties. The policy challenge is therefore not only to increase volume, but also to move the industry toward higher-value segments where margins, branding and regional differentiation are stronger.

Trade Performance, Exports and Imports

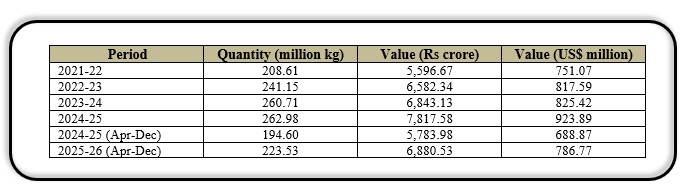

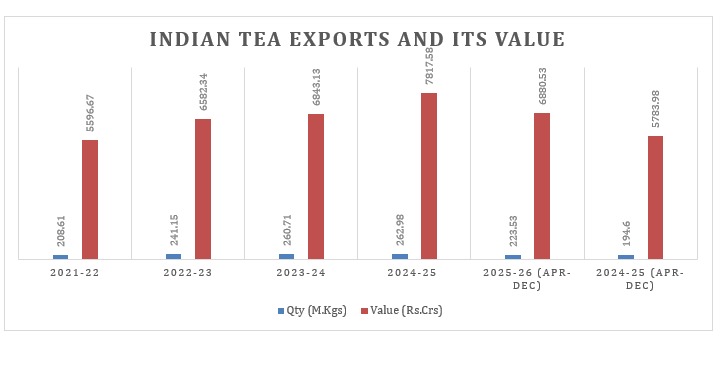

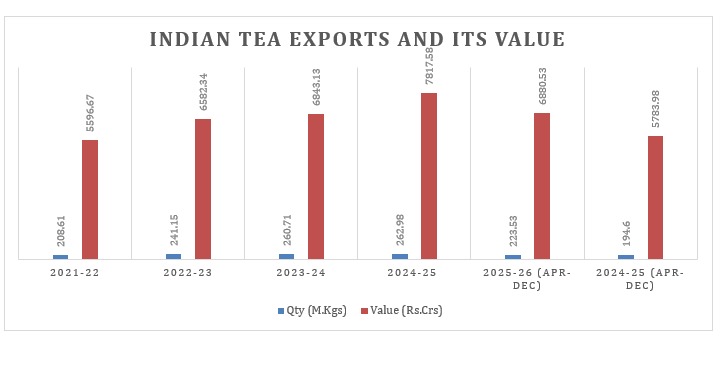

Tea exports have remained on an upward trajectory in recent years, with both volumes and values strengthening. In 2024-25, India exported 262.98 million kg of tea worth Rs 7,817.58 crore, or US$ 923.89 million. For the April-December period of 2025-26, exports reached 223.53 million kg worth Rs 6,880.53 crore. The rise in export value reflects not only quantity growth but also changes in product mix and pricing. India’s share in world tea exports in 2024 was 13.13 per cent, while its share in world tea production was 18.43 per cent.

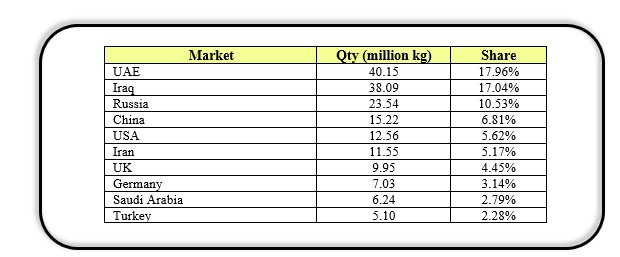

India’s tea exports are diversified across a broad set of markets, but a relatively small group of destinations accounts for most shipments. During April-December 2025-26, the United Arab Emirates, Iraq, Russia, China, the United States, Iran, the United Kingdom, Germany, Saudi Arabia and Turkey were among the leading destinations. Together, the top 20 markets accounted for 88.21 per cent of total exports, underscoring the importance of market concentration and targeted trade diplomacy.

Imports remain limited in relation to domestic production, generally at 2 to 3 per cent of total output, and are largely used for value addition and certain domestic requirements. Tea imports stood at 29.97 million kg in 2022-23, 25.21 million kg in 2023-24, 50.14 million kg in 2024-25 and 30.47 million kg in April-December 2025-26. Import management has therefore become a matter of both market balance and quality protection.

Prices, Value Realisation and Industry Economics

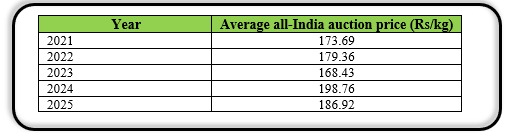

The tea market is highly sensitive to demand-supply conditions, weather, seasonal arrivals, quality differentials and international competition. Tea Board collects auction price data because the auction system remains a primary channel of sale. Under the Tea Marketing Control Order, producers are required to sell 50 per cent of their produce through public auctions licensed by the Board; the remaining volume may move through private sale, forward contracts or direct export. This framework gives the auction system a central role in price discovery.

Auction prices have fluctuated over the last five years, with a notable rise in 2024 followed by some moderation in 2025. This pattern reflects the interplay of supply conditions, quality availability and market sentiment. For the industry, price realisation is not merely a marketing question; it directly affects reinvestment capacity, replanting decisions, worker welfare expenditure and the ability of estates and growers to absorb rising input costs.

|

Do You Know? The tea economy is shaped by long-duration plantations, so cost pressures caused by ageing bushes, climate stress and labour shortages can persist for years unless structural interventions are taken early.

|

Government Schemes and Support Programmes

The principal ongoing instrument for sectoral support is the Tea Development and Promotion Scheme for the remaining period of the 15th Finance Commission cycle, covering 2023-24 to 2025-26. The scheme aims to raise production, productivity and quality, while also helping small tea growers move up the value chain. It gives special attention to the North Eastern States, exports to high-value markets, research and development, technological innovation and worker welfare. Its major components include plantation development and quality upgradation, tea promotion and market support, technological intervention, research and development, and welfare and capacity-building measures.

Support under the scheme is not limited to plantations. It includes the federation of small growers into self-help groups and farmer producer organisations, assistance for mini tea factories, soil testing, organic conversion and certification, farm field schools, awards for organised producer groups, capacity building and support for the education, health and social security needs of workers and their dependents. For closed gardens and gardens affected by natural calamities, the scheme also includes targeted educational support and aid for critically ill dependents.

The Board is also implementing the Pradhan Mantri Cha Shramik Protsahan Yojana for 2024-25 and 2025-26 in Assam and West Bengal, with a focus on tea garden workers, especially women and children. The scheme seeks to improve quality of life through infrastructure and asset creation with emphasis on health, education and shelter. Its components include Cha Shramik Shiksha Yojana, Cha Shramik Swasthya Suraksha Yojana and Cha Shramik Aashray Yojana. In Assam, the scheme has been operationalised through the State Level Committee mechanism, while implementation in West Bengal has been affected by the absence of an equivalent committee.

For the organised sector, support is also being provided for phased uprooting and replanting of old and unproductive bushes, adoption of mechanisation, use of renewable energy and other cost-saving technologies. For small growers, the policy emphasis is on collective action, better access to finance, improved agronomy and support for processing capacity closer to the farm gate.

Research, Quality Control and Innovation

Tea Board places strong emphasis on research because quality and productivity in tea are inseparable from scientific management. The Board supports research through the Darjeeling Tea Research and Development Centre, the Tea Research Association’s Tocklai Tea Research Institute, and the United Planters’ Association of South India’s Tea Research Foundation. These institutions work on agronomy, soil and water management, planting material improvement, pest and disease control, mechanisation, processing standardisation and value addition.

The Tea Board India pavilion at World Coffee Conference and Expo, Bengaluru, 25-28 September, 2023

Quality control is pursued through random sampling at manufacturing units, warehouses, importer premises and retail markets, against standards prescribed by the Food Safety and Standards Authority of India. Non-compliant samples are destroyed to prevent entry into the supply chain. This is a critical market protection mechanism because consumer trust in tea is highly dependent on safety, residue compliance and consistency.

The Board is also promoting geographical indication-based branding, especially for Darjeeling, Assam Orthodox, Nilgiri Orthodox and Kangra teas. Such branding initiatives reinforce the distinctiveness of Indian teas in premium markets. At the same time, Tea Board is developing a tamper-proof traceability system to track imported tea and reduce the risk of misuse or substitution. The system is being developed by C-DAC, Kolkata. The direction of innovation is clear: the industry is moving toward more data-driven oversight, better provenance assurance and stronger digital governance.

New technologies are also being explored for the field itself. These include IoT-based monitoring of water quality parameters such as dissolved oxygen, ammonia and turbidity, drone-based water sampling, mapping of floating macrophyte coverage, underwater fish-behaviour studies using remotely operated vehicles and space technology-based mapping of waterbodies. While these technologies were discussed in the source material as part of a broader scientific agenda, their relevance to tea lies in the sector’s growing interest in precision agriculture, environmental monitoring and digitally enabled supply-chain management.

Employment, Livelihoods and Social Impact

Tea remains one of India’s most socially consequential plantation industries. The organised sector employs 11.56 lakh workers, including permanent and temporary labour, while the wider tea ecosystem includes 2.49 lakh small tea growers and an additional 5 to 6 lakh persons in indirect and ancillary employment. This makes tea a major employer in remote and rural regions, where plantation wages and allied activities support local markets, transport, education, services and household consumption.

Darjeeling Tea Garden

The gender dimension is especially notable. Nearly 58 per cent of workers in the organised sector are women. This is one of the reasons worker welfare has remained central to tea policy. Under the Plantation Labour Act, estates are expected to provide housing, health services, education, social security and related amenities. The implementation of these obligations rests largely with the respective state governments, and the provisions of the Act are being subsumed under the labour codes now being brought into effect. In practical terms, tea policy has to balance productivity objectives with long-standing social responsibilities.

The rise of small tea growers has changed rural livelihoods in important ways. Small growers now account for 52 per cent of production, and many are being organised into self-help groups, farmer producer organisations and farmer producer companies. This collective architecture allows growers to access mechanisation, technical support and value-chain opportunities that would otherwise remain out of reach. It also creates a pathway toward mini tea factories and specialty tea production, potentially improving margins and regional entrepreneurship.

Environment, Sustainability and Climate Resilience

Tea is a perennial crop and a long-duration plantation asset, which means environmental stress accumulates over time. Climate change is already affecting the sector through erratic rainfall, droughts, flooding, rising temperatures, shifting humidity patterns, stronger pest and disease pressure and higher cost of production. These shocks reduce yields, disrupt plucking cycles, increase the need for plant protection measures and weaken the economics of cultivation. The source text correctly identifies climate adaptation as an immediate necessity rather than a distant objective.

Rolling tea plantations in Munnar, a renowned hill station located in the Western Ghats mountain range of Kerala, India.

Environmental sustainability in tea therefore requires a mix of replanting, soil health management, efficient water use, renewable energy, better estate design and organic or low-input practices where feasible. The Board is supporting organic conversion and certification for growers who can meet the relevant standards. It is also encouraging good agricultural practices and climate adaptation measures through training and capacity-building programmes. For the organised sector, the uprooting and replanting of ageing bushes is essential to maintain yield potential and quality over the long term.

Sustainability also has a spatial dimension. Tea cultivation in the North Eastern States, parts of West Bengal, the Nilgiris and the Himalayan foothills depends on fragile ecosystems and, in several cases, difficult logistics. Poor transport infrastructure, remoteness and weather vulnerability all raise costs. Protecting these regions requires both environmental prudence and supportive infrastructure so that growers can remain competitive without degrading the ecological base on which tea depends.

Marketing, Promotion and Brand Building

One of Tea Board’s core responsibilities is to promote Indian tea in domestic and international markets. The objective is not simply to sell more tea, but to position India as a dependable supplier of quality tea across categories such as whole leaf, CTC, green tea and specialty tea. Promotion is therefore deployed as a market-development instrument, a branding tool and a means of consumer education.

The formal observance of International Tea Day held on May 21, 2025, at Vanijya Bhawan, New Delhi.

Tea Board undertakes buyer-seller meets with importers in important markets, works with Indian embassies and missions, participates in major trade fairs such as World Food India, India International Trade Fair, Indus Food and AAHAR, and conducts outreach during International Tea Day and other occasions. It also promotes Indian teas through educational institutions, tea literacy initiatives, tasting zones and entrepreneurship programmes. Such activities help build familiarity with quality differences, regional origins and brewing practices.

Digital and out-of-home promotion has become a major feature of the Board’s public-facing strategy. Campaigns have been displayed at major airports, railway stations, metro systems, Vande Bharat trains, petrol pumps and flyovers. Tea Board also uses social media platforms such as X, Facebook and Instagram to disseminate product information, health-related content, recipes, quizzes and updates on Indian tea varieties. These campaigns are especially useful in markets where branding and consumer discovery matter as much as price.

On the trade facilitation side, the Board keeps the industry informed about export developments, market intelligence, logistics constraints and quality-related regulations. It also works to address market access issues such as residue limits and non-tariff barriers. In a more competitive and fragmented global market, these tasks are as important as field-level productivity interventions.

Challenges and Future Outlook

Despite its strengths, the tea sector faces a demanding future. Climate change has become the most persistent structural risk, but it is not the only one. Labour shortages, ageing bushes, higher pest pressure, residue management concerns, logistics bottlenecks, geopolitical disruptions, competition from lower-cost producers in Africa and South-East Asia and the persistence of non-tariff barriers all shape the industry’s economics. For many estates and growers, these challenges have translated into rising costs and tighter margins.

The future outlook is nevertheless constructive if the sector continues to move in the direction already visible in the source material. That means greater emphasis on quality assurance, phased replanting, mechanisation where suitable, renewable energy, stronger producer organisations, more specialty tea production, better organic and sustainable practices, and deeper investment in R&D and traceability. The industry’s opportunity lies in moving up the value chain: more value addition, more differentiated branding, and stronger positions in premium export and domestic segments.

Several broader reform themes emerge from stakeholder discussions. These include improving the efficiency and transparency of auctions, strengthening the price-sharing framework for small growers, deepening digital governance, improving worker welfare systems, expanding support for specialty teas and tea tourism, and reducing the friction caused by logistics and compliance bottlenecks. While these themes require further policy deliberation, they are aligned with the direction of sectoral reform suggested in the source material.

India’s tea future will therefore depend on a dual strategy. First, the country must protect the foundations of production through agronomic renewal, climate resilience and labour welfare. Second, it must treat tea as a brand-intensive, quality-sensitive and globally competitive product. The prize is significant: a stronger domestic market, a more resilient plantation economy, better incomes for growers and workers, and a larger share of the premium global tea trade.

|

Do You Know? India’s tea industry is more than 200 years old, yet its next phase of growth will depend on modern tools such as traceability systems, mechanisation, digital marketing and climate-smart agriculture.

|

Conclusion

The Indian tea sector remains one of the country’s most important plantation economies, linking rural livelihoods, export earnings, worker welfare and regional development. Tea Board of India sits at the centre of this ecosystem, combining regulatory oversight with promotion, research support, statistical intelligence and social policy functions. The sector’s present strength lies in its scale, diversity and resilience; its future strength will depend on its ability to adapt to climate risk, organise small growers, preserve quality and build stronger global brands. In that sense, Indian tea is not just a commodity. It is a living economic system that continues to evolve with science, policy and market demand.

References

Tea Board of India

Click here to download PDF

***

SSS/PK/……

(Explainer ID: 158446)

आगंतुक पटल : 319

Provide suggestions / comments