Ministry of Finance

INDUSTRIAL SECTOR GROSS VALUE ADDED (GVA) ROSE BY 3.7 PER CENT IN FIRST HALF OF FY23

PRIVATE FINAL CONSUMPTION EXPENDITURE (PFCE) AS A SHARE OF GDP IN H1 OF FY23 WAS HIGHEST AMONG ALL HALF YEARS SINCE FY15

FDI INFLOW AT US$ 21.3 BILLION IN FY22 MARKING 76 PER CENT RISE FROM FY21

INDIAN PHARMACEUTICAL EXPORTS ACHIEVED 24 PER CENT GROWTH IN FY21

CUMULATIVE FDI IN PHARMA SECTOR CROSSED US$ 20 BILLION MARK BY SEPTEMBER 2022

COAL PRODUCTION FOR FY23 ESTIMATED TO INCREASE TO 911 MILLION TONNES

INDIA IS NOW THE 3RD LARGEST AUTOMOBILE MARKET

INDIA IS 2ND LARGEST MOBILE PHONE MANUFACTURER GLOBALLY

CREDIT TO INDUSTRY GROWING, PARTICULARLY FOR MSMEs

PLI SCHEME EXPECTED TO ATTRACT CAPEX OF APPROX ₹4 LAKH CRORE OVER THE NEXT FIVE YEARS

INDUSTRY 4.0 IS INDIA’S WAY FORWARD IN ACHIEVING THE GOALS OF AATMANIRBHARTA AND AMBITIONS OF BECOMING A KEY PLAYER IN GLOBAL VALUE CHAINS

प्रविष्टि तिथि:

31 JAN 2023 1:41PM by PIB Delhi

The Overall Gross Value Added (GVA) by the Industrial Sector rose 3.7 per cent, based on data available for the first half of the FY23, which is higher than the average growth of 2.8 per cent achieved in H1 of the last decade, stated the Economic Survey 2022-23 presented by the Union Minister for Finance & Corporate Affairs Smt. Nirmala Sitharaman in Parliament today.

OVERVIEW OF INDUSTRIAL SECTOR

Economic Survey tabled in the Parliament stated that Industry sector witnessed modest growth of 4.1 per cent in FY23 compared to the strong growth of 10.3 per cent in FY22. It explained that this is likely on account of input cost-push pressures, supply chain disruptions and the China lockdown impacting the availability of essential inputs and slowing the global economy.

The Survey highlighted that the PLI schemes are set to unlock manufacturing capacity, boost exports, reduce import dependence and lead to job creation for both skilled and unskilled labour. The Survey was optimistic that easing input prices and conducive demand conditions will support overall Industrial growth.

DEMAND STIMULUS TO INDUSTRIAL GROWTH

Private Final Consumption Expenditure (PFCE) as a share of GDP in H1 of FY23 was the highest among all half years, H1 or H2, since FY15, the Survey stated. The Survey optimistically expressed that with world commodity prices on a downward trajectory and showing up in declining rates of India’s wholesale inflation, core retail inflation is expected to relent, making domestic consumption demand much stronger to further induce industrial growth in the country.

Economic Survey stated that the strong export performance of FY22 continued somewhat in the first half of FY23 while exports of goods and services as a share of GDP have been the highest since FY16 during H1 of FY23.

The Survey warned that export growth may slow further in the second half of the current financial year and remain weak beyond that, too, if the global economy falls into recession. It added that however, the strong domestic consumption growth and investment revival is expected to keep industrial production humming.

The Survey emphasized that New Investment announced in the manufacturing sector during April-December of FY23 was five times the corresponding level in FY20. The Survey analyzed this increase in investment demand was triggered by the augmented capex of the central government in the current and the previous year as compared to the pre-pandemic years. The leap also has crowded in private investment, already upbeat on the pent-up demand, export stimulus, and strengthening of the corporate balance sheets. It added that Capacity utilization in the manufacturing sector has been rising which bodes well for new investment activity in creating additional capacity.

SUPPLY RESPONSE OF INDUSTRY

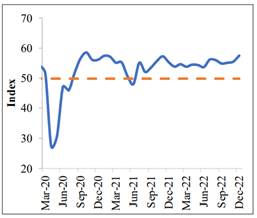

Purchaser’s Manufacturing Index (PMI) manufacturing has remained in the expansion zone for 18 months since July 2021, and its sub-indices indicate an easing of input cost pressures, improving supplier delivery times, robust export orders, and future output, highlighted the Survey.

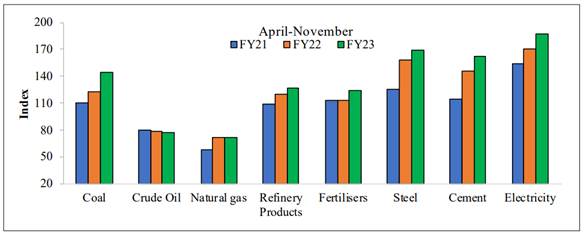

The Survey noted the growth of the eight core industries of coal, fertilizers, cement, electricity, steel, and refinery products has held steady, reflecting a broad momentum in industrial activity.

The Survey added that while growth in the consumer durables component of the Index of Industrial Production (IIP) is on account of the release of ‘pent-up’ demand, the increase in capital goods and infrastructure/ construction goods is indicative of the beginnings of a virtuous investment cycle that is expected to be led by the private sector.

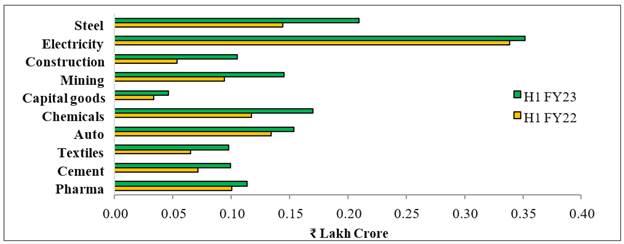

ROBUST GROWTH IN BANK CREDIT TO INDUSTRY

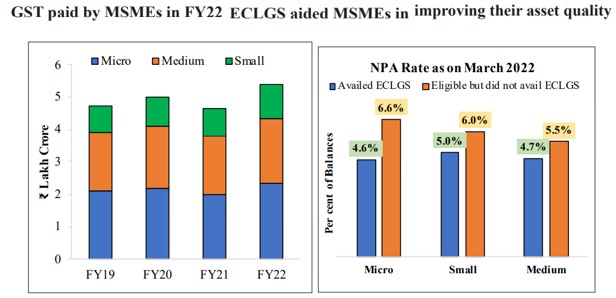

The Survey highlighted that the credit to industry started recovering from January 2022 and has been growing in double digits since July 2022. It added that Credit to MSMEs has also seen a significant increase in part, assisted by the introduction of the Emergency Credit Linked Guarantee Scheme (ECLGS).

The Survey stated that the impact of ECLGS on increasing the growth of credit to MSME was felt most during the pandemic impacted years of 2020 and 2021. It continued in 2022 as the scheme was extended to March 2023.

Further it added, growth in credit to MSME was buttressed by rebounding consumption levels, particularly in the services sector. Consequently, the share of MSMEs in gross credit offtake to the industry rose from 17.7 per cent in January 2020 to 23.7 per cent in November 2022.

The Survey expressed that robust growth in credit demand combined with rising capacity utilization and investment in manufacturing underscores businesses’ optimism regarding future demand.

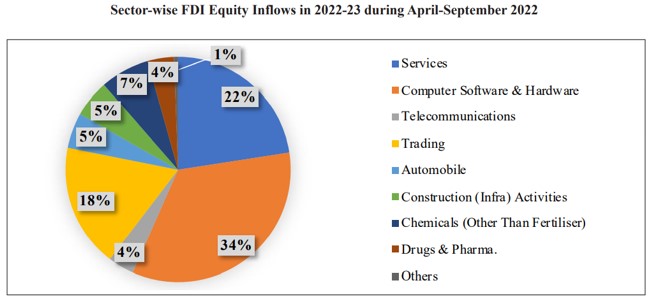

RESILIENT FDI INFLOW IN MANUFACTURING SECTOR

The Survey highlighted that the FDI inflow jumped to US$ 21.3 billion in FY22 from US$ 12.1 billion in FY21 as the pandemic-driven expansionary policies of advanced economies led to a surge in global liquidity.

The Survey mentioned that FDI equity inflow in manufacturing in the first half of FY23 fell below its corresponding level in the first half of FY22, with the rise in global uncertainty in the wake of the Russia-Ukraine conflict.

A rebound in FDI inflows is, however, expected as the Indian economy sustains its high growth while monetary tightening the world over eventually eases with the weakening of inflationary pressures, the Survey expressed optimism.

HIGHLIGHTS OF INDUSTRY GROUPS

- MICRO, SMALL AND MEDIUM ENTERPRISES (MSMEs)

The Survey noted that the MSME contribution to the manufacturing sector’s GVA also marginally fell to 36.0 per cent in FY21. The Survey further emphasized that the AatmaNirbhar Bharat Package by the Government provided cushion to the economic impact of the pandemic on MSMEs, which has helped post smart recovery from pandemic.

The Survey expressed that the recovery of the MSME sector from the pandemic-induced shock is evident in the trend in GST paid by the units of MSME sector in FY22 has crossed the pre-pandemic level in FY20.

Government’s initiative of the Samadhaan Portal, CHAMPIONS:the single-window grievance redressal portal for MSMEs, Trade Receivables Discounting System (TReDS) platform for facilitating the discounting of trade receivables of MSMEs with a turnover of ₹200 crore or more, ‘Raising and Accelerating MSME Performance’ scheme (RAMP) etc. has helped in strengthening the MSMEs stated the Economic Survey.

- ELECTRONICS INDUSTRY

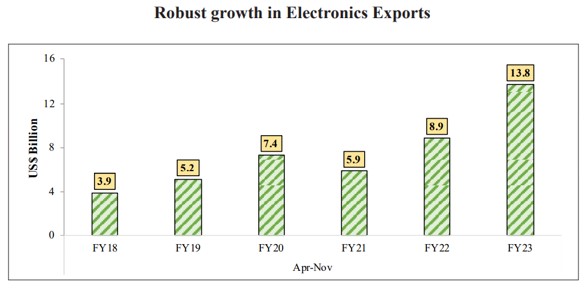

The Survey emphasized that Electronic goods were among the top five commodity groups exhibiting positive export growth in November 2022, with the exports in this segment growing YoY by 55.1 per cent.

Elaborating on the Electronics industry, the Survey stated that major drivers were mobile phones, consumer electronics and industrial electronics. It highlighted that India has become the second-largest mobile phone manufacturer globally, with the production of handsets going up from six crore units in FY15 to 31 crore units in FY22.

The Survey also mentioned that various initiatives and incentives of Government like PLI scheme for Large Scale Electronics Manufacturing, the PLI scheme for IT hardware, the Scheme for Promotion of Manufacturing of Electronic Components and Semiconductors (SPECS) has nurtured and enhanced the electronics manufacturing base.

Additionally, under the Programme for Development of Semiconductors and Display Manufacturing Ecosystem in India, the Cabinet approved the comprehensive development of a sustainable semiconductor and display ecosystem in the country with an outlay of ₹76,000 crore.

- COAL INDUSTRY

The coal production for FY23 is estimated to increase to 911 million tonnes, about 17 per cent higher compared to the previous year, highlighted the Survey. Consequent to the well-timed measures of the Government, India has been placed in a better position to cater to excess energy demand. It further added that the coal industry is expected to grow at 6-7 per cent annually to reach a production level of 1 billion tonnes by FY26 and about 1.5 billion tonnes by 2030.

- STEEL INDUSTRY

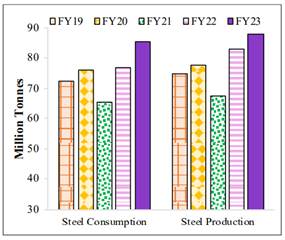

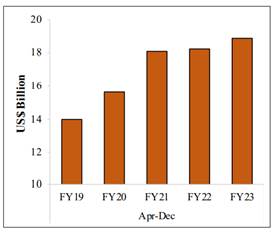

Economic Survey highlighted the steel sector’s performance in the current fiscal year as robust, with cumulative production and consumption of finished steel at 88 MT and 86 MT, respectively, during April-December 2022, higher than the corresponding period during the previous four years.

The Survey stated that iron and steel exports are higher by 20 per cent over the corresponding pre-pandemic levels of FY20, despite moderation in the first eight months of the current fiscal owing to a slowdown in the global economy.

Increasing Steel production and Consumption (Apr-Dec)

- TEXTILE INDUSTRY

In the current financial year, the textile industry has been facing the challenge of moderating exports compared to FY22, mentioned the Survey. It added that export of readymade garments registered a growth of 3.2 per cent YoY basis during the same period.

The Government approved the setting up of seven PM Mega Integrated Textile Region and Apparel (PM MITRA) Parks and launched the Textile PLI Scheme with an approved outlay of ₹10,683 crore over five years starting from 1st January 2022 to promote investments. These would help to develop integrated large-scale and modern industrial infrastructure facilities for the entire value chain of the textile industry, the Survey stated.

- PHARMACEUTICALS INDUSTRY

The Survey highlighted that Indian pharmaceutical exports achieved a healthy growth of 24 per cent in FY21. It expressed hope that India’s domestic pharmaceutical market is estimated to grow to US$ 65 billion by 2024 from estimated US$ 41 billion in 2021 and is further expected to reach US$ 130 billion by 2030.

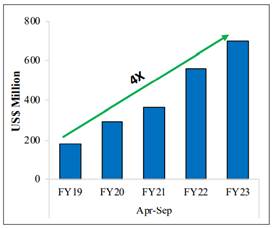

Strong Growth in pharma exports High Inflow of FDI in Pharma sector

Carrying forward this growth momentum, drug and pharmaceutical exports during April-October 2022 was 22 per cent higher than the corresponding pre-pandemic period of FY20, noted the Survey. It added that Cumulative FDI in the pharma sector crossed the US$ 20 billion mark in September 2022 and FDI inflows have increased four-fold over five years until September 2022, to US$ 699 million, supported by investor-friendly policies and a positive outlook for the industry.

- AUTOMOBILE INDUSTRY

India became the 3rd largest automobile market, surpassing Japan and Germany in terms of sales, in December 2022, stated the Economic Survey. It added that in 2021, India was the largest manufacturer of two-wheeler and three-wheeler vehicles and the world’s fourth-largest manufacturer of passenger cars.

Elaborating on the domestic electric vehicles (EV) market, the Survey stated that it is expected to grow at a compound annual growth rate (CAGR) of 49 per cent between 2022 and 2030 and is expected to hit one crore units annual sales by 2030. It added that the EV industry will create 5 crore direct and indirect jobs by 2030.

FOSTERING INNOVATION

Economic Survey stated that there was a 46 per cent growth in the domestic filing of patents over 2016-2021, signaling India’s transition towards a knowledge-based economy.

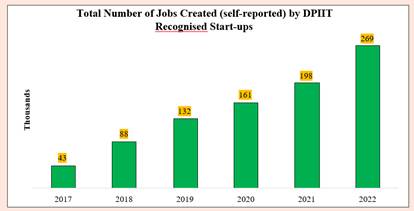

Discussing the achievements of Start-ups, the Survey highlighted that an impressive 9 lakh+ direct jobs have been created by the DPIIT recognized startups (self-reported), with a notable 64 per cent increase in 2022 over the average number of new jobs created in the last three years. About 48 per cent of our startups are from Tier II & III cities, a testimony of our grassroots’ tremendous potential.

INDUSTRY 4.0

The Survey highlighted that adoption of Industry 4.0 technologies such as cloud computing, IoT, machine learning, and artificial intelligence (AI) in the Indian manufacturing sector is underway, however, large-scale adoption is yet to happen and an enabling environment is rapidly developing.

The Survey mentioned that various Government Initiatives such as SAMARTH (Smart Advanced Manufacturing and Rapid Transformation Hubs) Udyog Bharat 4.0, establishment of the Centre for Fourth Industrial Revolution is the way forward in achieving the goals of Aatmanirbharta and its ambitions of becoming a key player in global value chains.

MAKE IN INDIA 2.0

The Survey mentioned that ‘Make in India 2.0’ is now focusing on 27 sectors, which include 15 manufacturing sectors and 12 service sectors. Amongst these, 24 sub-sectors have been chosen while keeping in mind the Indian industries’ strengths and competitive edge, the need for import substitution, the potential for export and increased employability.

PERFORMANCE LINKED INCENTIVE (PLI) SCHEME

PLI scheme is expected to attract a capex of approximately ₹4 lakh crore over the next five years having a potential of generate employment for over 60 lakh in India stated the Economic Survey. It added that Sectors under which the PLI scheme has been announced currently constitute around 40 per cent of the total imports. The scheme, spread across 14 sectors, can enhance India’s annual manufacturing capex by 15 to 20 per cent from FY23.

The Survey mentioned that around ₹47,500 crore (US$ 6 billion) of actual investment has been made (As per recent reporting from implementing Ministries/ Departments); production/ sales of ₹3.85 lakh crore (US$ 47 billion) of eligible products and employment generation of around 3 lakh has been reported and 106 per cent achievement of actual investment reported versus the corresponding projections of FY22.

The Survey stated that more than 100 MSMEs are among the PLI beneficiaries in sectors such as Bulk Drugs, Medical Devices, Telecom, White Goods and Food Processing. Key sectors such as Large-Scale Electronics Manufacturing, Pharmaceuticals, Telecom & Networking Products, Food Processing and White Goods have contributed considerably to investment, production, sales and employment.

*******

RM/PPG/SR

(रिलीज़ आईडी: 1894918)

आगंतुक पटल : 24586