Ministry of Finance

A Decade of Growth with PM Mudra Yojana

Fueling grassroots entrepreneurship and expanding financial inclusion

Posted On:

07 APR 2025 4:44PM by PIB Delhi

Introduction

On 8 April 2025, India marks 10 years of the Pradhan Mantri MUDRA Yojana (PMMY). Pradhan Mantri Mudra Yojana (PMMY), the Flagship Programme of the Prime Minister aimed at Funding the Unfunded micro enterprises and small businesses. By removing the burden of collateral and simplifying access, MUDRA laid the foundation for a new era of grassroots entrepreneurship.

Across the country, lives have transformed. Kamlesh, a home-based tailor in Delhi, expanded her work, employed three other women, and enrolled her children in a good school. Bindu, who began with 50 brooms a day, now leads a unit producing 500. These are not exceptions anymore. They reflect a larger shift.

From stitching units and tea stalls to salons, mechanic shops, and mobile repair businesses, crores of micro-entrepreneurs have stepped forward with confidence, enabled by a system that believed in their potential. PMMY has supported these journeys by offering institutional credit to non-corporate, non-farm micro and small enterprises that form the backbone of India’s economy.

At its core, the MUDRA Yojana is a story of trust. Trust in people’s aspirations and in their ability to build. Trust in the belief that even the smallest dreams deserve a platform to grow.

Achievements under Pradhan Mantri Mudra Yojana

Since its launch in April 2015, the Pradhan Mantri Mudra Yojana (PMMY) has sanctioned over 52 crore loans worth ₹32.61 lakh crore, fuelling a nationwide entrepreneurial revolution. Business growth is no longer confined to big cities—it is spreading to small towns and villages, where first-time entrepreneurs are taking charge of their destinies. The shift in mindset is evident: people are no longer job seekers; they are becoming job creators.

MSME Credit Boom: A Stronger Business Ecosystem

The SBI report highlights a significant rise in credit flow to MSMEs, driven by Mudra’s impact. MSME lending surged from ₹8.51 lakh crore in FY14 to ₹27.25 lakh crore in FY24, and is projected to cross ₹30 lakh crore in FY25. The share of MSME credit in total bank credit increased from 15.8 percent in FY14 to nearly 20 percent in FY24, showcasing its growing role in the Indian economy. This expansion has enabled businesses in smaller towns and rural areas to access financial support that was previously unavailable, strengthening India’s self-reliant economy and driving grassroots job creation.

Financial Inclusion: Empowering Women

Women account for 68 percent of all Mudra beneficiaries, underscoring the scheme’s pivotal role in advancing women-led enterprises across the country. Between FY16 and FY25, the per woman PMMY disbursement amount increased at a CAGR of 13 percent, reaching ₹62,679, while per woman incremental deposits grew at a CAGR of 14 percent to ₹95,269. States with higher disbursement shares to women have recorded significantly higher employment generation through women-led MSMEs, reinforcing the effectiveness of targeted financial inclusion in enhancing women’s economic empowerment and labour force participation.

Financial Inclusion: Reaching Socially Marginalised Groups

PMMY has made significant progress in breaking traditional credit barriers. According to the SBI report, 50 percent of Mudra accounts are held by SC, ST and OBC entrepreneurs, ensuring wider access to formal finance. Furthermore, 11 percent of Mudra loan holders belong to minority communities, demonstrating the scheme’s contribution to inclusive growth by enabling marginalised communities to become active participants in the formal economy.

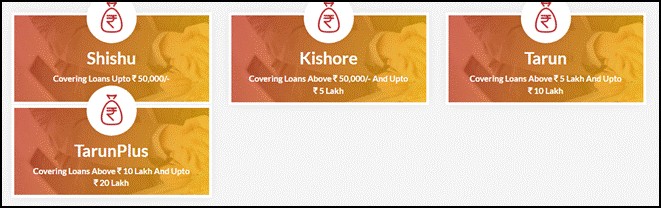

Progressive Lending: From Shishu to Tarun

Over the past ten years, Mudra has facilitated the opening of over 52 crore loan accounts, marking a steady rise in entrepreneurial activity. The share of Kishor loans (₹50,000 to ₹5 lakh) has grown from 5.9 percent in FY16 to 44.7 percent in FY25, indicating a shift from micro to small enterprises. The Tarun category (₹5 lakh to ₹10 lakh) is also gaining momentum, proving that Mudra is not just about starting businesses but helping them scale.

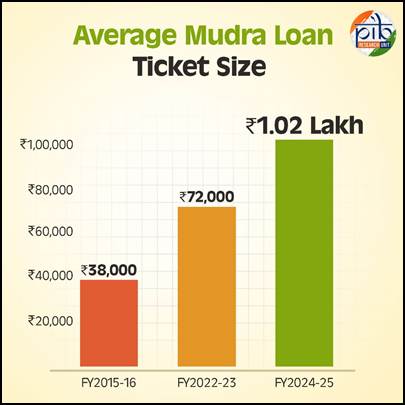

Bigger Loans, Stronger Businesses

A telescopic view of total loans sanctioned and disbursed under PMMY reveals that the scheme’s Unique Selling Proposition has been well received by a diverse base of intended beneficiaries, thereby strengthening the economic influence of the bottom of the pyramid.

The average ticket size of loans has nearly tripled—rising from ₹38,000 in FY16 to ₹72,000 in FY23, and further to ₹1.02 lakh in FY25—reflecting growing economies of scale and a deepening of both market depth and width.

Furthermore, loan disbursal rose by 36 percent in FY23, indicating a strong revival of entrepreneurial confidence across the country.

Leading States/UTs in PM Mudra Loan Disbursal

As of February 28, 2025, since the launch of the Pradhan Mantri Mudra Yojana in 2015, Tamil Nadu has recorded the highest disbursal among states at ₹3,23,647.76 crore. Uttar Pradesh follows with ₹3,14,360.86 crore, while Karnataka ranks third with ₹3,02,146.41 crore. West Bengal and Bihar have also seen significant disbursals of ₹2,82,322.94 crore and ₹2,81,943.31 crore respectively. Maharashtra stands sixth at ₹2,74,402.02 crore, reflecting the scheme’s broad reach and impact across key states over the past decade.

Among Union Territories, Jammu and Kashmir leads with a total disbursal of ₹45,815.92 crore across 21,33,342 loan accounts. The figures underscore the role of the scheme in expanding access to credit

and promoting self-employment, not just across states but also in Union Territories.

Click here for the complete list.

Funding the Unfunded

Micro enterprises constitute a major economic segment in our country and provides large employment after agriculture. This segment includes micro units engaged in manufacturing, processing, trading and services sector. It provides employment to nearly 10 crore people. Many of these units are proprietary/ single ownership or Own Account enterprises and many a time referred as Non-Corporate Small Business sector.

Mission, Vision and Purpose of PMMY

Salient Features of the Scheme

Pradhan Mantri Mudra Yojana (PMMY) under the Micro Units Development and Refinancing Agency (MUDRA) was set up by Government of India for development and refinancing activities relating to micro units. PMMY ensures collateral-free institutional credit up to Rs 20 lakh is provided by Member Lending Institutions (MLIs) i.e. Scheduled Commercial Banks (SCBs), Regional Rural Banks (RRBs), Non-Banking Financial Companies (NBFCs) and Micro Finance Institutions (MFIs).

Under the scheme, three categories of interventions have been formulated which include:

|

Tarun Plus: Loans above ₹10 lakh and up to ₹20 lakh (designed specifically for Tarun category, who have previously availed and successfully repaid loans)

|

International Recognition

The International Monetary Fund (IMF) has consistently acknowledged the impact of the Pradhan Mantri Mudra Yojana (PMMY) in expanding financial access and promoting inclusive entrepreneurship in India.

In 2017, the IMF noted that the scheme has been instrumental in enabling women-led businesses to access finance. It highlighted how PMMY complements PMJDY’s focus on unbanked households by providing collateral-free loans to micro, small, and medium-sized businesses.

In 2019, the IMF further praised PMMY, stating that the scheme under the Micro Units Development and Refinance Agency plays a vital role in developing and refinancing micro enterprises by supporting financial institutions that lend to businesses engaged in manufacturing, trading and services.

By 2023, the IMF highlighted that the collateral-free loan structure of PMMY, with its emphasis on women’s entrepreneurship, has significantly contributed to the growth of women-owned MSMEs, which now exceed 2.8 million.

In its 2024 release, the IMF reaffirmed that India’s enabling policy environment for entrepreneurship, through programmes such as PMMY, is actively contributing to increased self-employment and formalisation through credit access.

Conclusion

In ten years, Pradhan Mantri Mudra Yojana has consistently demonstrated the power of financial inclusion and the strength of grassroots innovation. Before 2014, access to credit often favoured the well-connected, while small entrepreneurs faced hurdles like complex paperwork or were forced to rely on informal finance. Banks handed out reckless loans to large corporates, while genuine borrowers lost access to credit. MUDRA stepped into this vacuum, offering a cleaner, inclusive alternative that gave everyone an equal chance.

With over 52 crore loans sanctioned, the scheme has empowered women, SC/ST/OBC communities, and rural entrepreneurs by expanding access to formal credit. The rise in average loan size, growing share of MSME credit, and the shift from micro to small enterprises reflect its growing impact. PMMY is not only fuelling self-employment and job creation, but also strengthening India’s grassroots economy and advancing equitable growth.

References

Click here to see PDF.

*****

Santosh Kumar/ Sarla Meena/ Anchal Patiyal

(Release ID: 2119781)

Visitor Counter : 978