Economy

GST Simplified: Clearing Your Doubts Before the New Rates Kick In

Posted On:

21 SEP 2025 12:59PM

1. What is GST?

GST (Goods and Services Tax) is a single indirect tax on the supply of goods and services across India. It replaces multiple taxes like excise, VAT, and service tax, creating one unified market.

2. From when will the revised GST rates come into effect?

The new GST rates will apply from 22nd September, 2025, as recommended by the GST Council.

3. What has changed in GST from 22nd September, 2025?

From this date, revised GST rates on several goods and services come into effect, based on the GST Council’s decisions. The changes aim to simplify rates, remove anomalies, and make the system easier for both businesses and consumers.

4. Will GST registration rules change from 22nd September, 2025?

No. The threshold limits for GST registration remain the same. Only the tax rates on certain supplies are being revised.

5. Which notification will notify the revised GST rates?

The changes will be notified through official rate notifications issued by the Government. These notifications are available on the CBIC website.

6. What will be the applicable rate of tax if goods or services were supplied before the GST rate change, but the invoice was issued later?

In such cases, the “time of supply” rules under Section 14 of the CGST Act will decide the applicable rate. If both supply and payment were made before 22nd September, the earlier rate will apply. However, if supply was before but invoice or payment comes after 22nd September, the revised rate will be charged.

7. What GST rate will apply if advances were received before the rate change but the supply or invoice is issued later?

The rate depends on the timing of the advance. Advances received before 22nd September will be taxed at the old rate. If the advance is received on or after 22nd September, or if the supply is completed later, GST will apply at the revised rate.

8. Will e-way bills need to be cancelled and reissued for goods in transit when the new GST rates take effect?

No. E-way bills issued before the rate change remain valid for their full duration. Goods already in movement with a valid e-way bill do not need a fresh bill after 22nd September.

9. If I already hold stock on the date of the rate change, should I apply the revised rate on supply?

Yes. GST is charged on the date of supply, not on the date of purchase. So, even if the stock was purchased earlier, any supply made on or after 22nd September will attract the new rate.

10. What will happen to ITC on purchases made before the change in GST rates? Will you get ITC at reduced rate now?

You can claim full ITC (Input Tax Credit) on purchases made before the rate change, as long as GST was charged correctly at that time. The later change in rates will not reduce the credit already available to you. In short, whatever tax you paid earlier remains valid credit in your GST ledger.

11. My outward supply is exempt under the new rate schedule, but I already have ITC in my ledger. Do I need to reverse it?

You can use the ITC balance for supplies made up to 21st September, 2025. But from 22nd September, once your supply becomes exempt, the ITC related to it cannot be used and must be reversed as per GST rules.

12. Will I be allowed to claim refund of accumulated credit under inverted duty structure for supplies made up to the effective date of the revised rate?

No. Refund of accumulated ITC under inverted duty is available only where inputs are permanently taxed at a higher rate than outputs. If the difference is only because of a rate change over time on the same goods, refund is not allowed.

13. Which life insurance policies are covered under the GST exemption?

The exemption applies to all individual life insurance policies, including term plans, endowment policies, and ULIPs. Reinsurance of these individual policies is also exempt.

14. Which health insurance policies are covered under the GST exemption?

Individual health insurance policies, including family floater and senior citizen plans, are exempt from GST. Reinsurance of such individual policies is also exempt under this decision.

15. In addition to exempting individual health and life insurance services, will any input services of insurers also be exempted?

Only reinsurance services are exempt. Other inputs such as commissions and brokerage remain taxable, and insurers cannot claim ITC on them once the output supply is exempt. Such ITC will have to be reversed.

16. Will passenger transportation services be taxed at 18%?

No. Passenger transport by road will continue at 5% without ITC, though operators may opt for 18% with ITC. In the case of air travel, economy class is taxed at 5%, while other classes remain at 18%.

17. What is the applicable GST rate on multimodal transport of goods?

If the multimodal transport does not include any air leg, it is taxed at 5% with limited ITC (restricted to 5% of the value). If any portion involves air transport, the applicable rate is 18% with full ITC.

18. Who is liable to pay GST on local delivery services provided through an ECO?

If local delivery services are provided through an e-commerce operator (ECO) by an unregistered person, the e-commerce operator is responsible for paying GST. If the service provider is registered, then that provider is liable to pay the tax.

19. What is the GST rate applicable on local delivery services?

Local delivery services are taxed at 18%. If the supplier is registered, the supplier pays GST. If the supplier is unregistered and provides services through an e-commerce platform, the operator pays GST.

20. Are local delivery services provided through an ECO covered under the scope of GTA?

No. Local delivery services through e-commerce platforms are not considered as Goods Transport Agency (GTA). They are treated as a separate category of service.

21. Is it necessary to recall and re-label the MRP on medicines already in the supply chain before 22nd September, 2025? How will the re-labelling be carried out?

No recall of stock is required. Manufacturers only need to issue revised price lists and share them with dealers, retailers, and regulators. Stock already in the market can continue to be sold, provided billing reflects the new prices.

22. Why haven’t all medicines been fully exempted from GST?

Exempting medicines would prevent manufacturers from claiming ITC on raw materials and inputs, raising their production costs. These costs would eventually be passed on to consumers. Keeping medicines at a concessional 5% rate (except those specified at nil rate) ensures affordability while allowing ITC to flow through the supply chain.

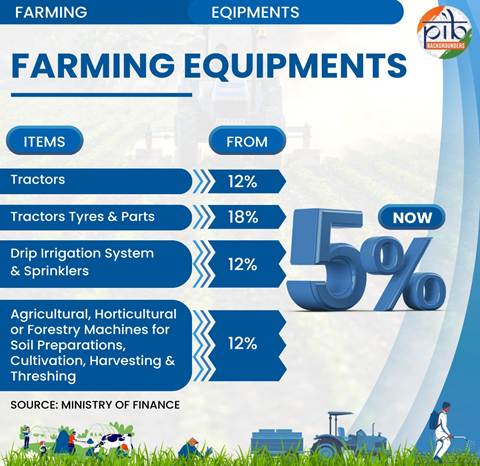

23. Why hasn’t agricultural machinery been fully exempted from GST?

If agri-machinery is made fully tax-free, manufacturers lose input tax credit on raw materials, raising their costs. These higher costs would be passed on to farmers, making machinery more expensive. Hence, it is kept taxable at a concessional rate to balance relief for farmers and viability for manufacturers.

24. Why hasn’t GST been removed on raw cotton?

Cotton is taxed under reverse charge, so farmers do not pay GST directly. This system keeps the input tax credit chain intact for the textile industry, which helps keep costs stable and benefits consumers.

25. Will technical textiles like geotextiles and agro-textiles face greater inversion since they mainly use plastic components such as polyethylene and polypropylene?

Technical textiles like geotextiles and agro-textiles are treated as textiles, not plastics, under the international classification system adopted by India. While some inversion may remain, GST allows refund of accumulated input credit in such cases. With process reforms, these refunds will be processed faster, ensuring that manufacturers are not burdened.

26. What is the tax treatment for leasing or renting services without an operator?

Majority of leasing or renting without operator is taxed at the same rate as the goods themselves. For example, if a car is taxed at 18%, then renting or leasing that car without a driver is also taxed at 18%. The same rule applies to other goods, the tax on renting matches the tax on buying.

27. Will the revised GST rates also apply to imported goods?

Yes. IGST on imports will be levied at the revised GST rates from 22nd September, except where a specific exemption has been provided.

28. UHT (Ultra High Temperature) milk has been exempted. Does this exemption also apply to plant-based milk?

No. The exemption is only for dairy UHT milk. Plant-based milk drinks (like almond milk) earlier attracted 18% GST, and soya milk drink 12%. Now all plant-based milk drinks, including soya milk, will be taxed at 5%.

29. Why has GST on face powders and shampoos been reduced, and will this not also benefit MNCs and luxury brands?

Face powders and shampoos are common household items used across all sections of society. While premium or luxury brands will also see the benefit, the main purpose of the rate cut is to simplify the GST system. Having separate rates based on brand or price would make the tax structure complicated and difficult to administer.

30. Why is refund of inverted duty on imitation zari made from metallised plastic film restricted, while no such restriction applies to other textile products made from plastic or rubber?

The GST Council had already decided in its 52nd meeting to restrict refunds on imitation zari made from metallised plastic film. The current exercise is only to simplify and streamline GST rates, so that earlier decision continues.

References

https://www.pib.gov.in/PressReleasePage.aspx?PRID=2163560

https://www.pib.gov.in/PressReleasePage.aspx?PRID=2167151

GST Simplified: Clearing Your Doubts Before the New Rates Kick In

*****

SK/M

(Explainer ID: 155252)

आगंतुक पटल : 25391

Provide suggestions / comments

इस विज्ञप्ति को इन भाषाओं में पढ़ें:

हिन्दी