Others

15 September 2025 : ITR Deadline What Every Taxpayer Should Know

Posted On: 07 SEP 2025 9:33AM

Key Takeaways

- The last date to file Income Tax Returns (ITR) for FY 2024–25 (AY 2025–26) is 15 September 2025.

- Filing is now simpler with pre-filled forms and faster online processing.

- Over 7.28 crore ITRs were filed in AY 2024–25, showcasing rising digital adoption.

- Late filing attracts penalties and interest charges.

- File online at www.incometax.gov.in with pre-filled details and simple Aadhaar OTP verification.

|

Introduction

The 15 September 2025 deadline (extended from the usual 31 July) is for non-audit cases. This includes filers under ITR‑1 to ITR‑4.

|

Filing an Income Tax Return (ITR) is an important compliance requirement under the Income Tax Act. It enables individuals and entities to declare their income, report taxes paid, and claim refunds where applicable. Timely filing helps avoid penalties, ensures faster processing of refunds, and also serves as an official financial record for availing loans, obtaining visas, and fulfilling other financial requirements.

For FY 2024–25 (AY 2025–26), the Central Board of Direct Taxes (CBDT) has extended the due date for non-audit taxpayers, including most individuals, Hindu Undivided Family (HUFs), and other entities not subject to audit, to 15 September 2025.

A non-audit case is when a taxpayer’s accounts are not required to be audited under the Income Tax Act. This generally includes:

- Individuals and HUFs with income from salary, pension, house property, capital gains, or other sources.

- Small businesses and professionals who opt for the presumptive taxation scheme (Sections 44AD, 44ADA, 44AE) and whose turnover does not cross the limit requiring audit

Financial Year (FY):

The Financial Year is the year in which you earn your income. For example, if you earn income between 1 April 2024 and 31 March 2025, that period is called Financial Year 2024–25 (FY 2024–25).

Assessment Year (AY):

The Assessment Year is the year immediately after the Financial Year, in which you file your Income Tax Return (ITR) and the government assesses (checks) the income earned in the previous year. For example, income earned in FY 2024–25 will be reported and assessed in Assessment Year 2025–26 (AY 2025–26).

|

What is ITR and Who Should File?

An ITR (Income Tax Return) is a form to declare your income and taxes. You should file if:

- Your income is above the basic exemption limit.

- You want to claim refunds (for excess TDS deducted).

- You need proof of income for bank loans, visa applications, or financial transactions.

|

Filing ITR goes beyond a statutory requirement and plays a vital role in strengthening both personal financial credibility and the nation’s economy. It reflects rising incomes, employment, and the growing formalisation of the economy. For individuals, regular filing helps build creditworthiness, which is essential for availing loans, securing visas, and entering business contracts. It also enables taxpayers to claim refunds for excess taxes paid and ensures the carry-forward of losses for future setoffs.

For the government, ITR data is an important tool for policy planning, subsidy targeting, and broadening the tax base. It provides valuable insights into income patterns and economic activity, aiding in better governance. Subsequently, timely and accurate ITR filing contributes to a transparent, documented, and accountable economy, strengthening both compliance and financial inclusion.

A late filing fee is levied if the return is furnished after the specified due date. A fee of ₹5,000 is payable for returns filed after the due date. However, in cases where the total income does not exceed ₹5 lakh, the late fee is restricted to ₹1,000.

In addition, a delay in filing attracts 1% interest per month on the pending tax amount, in addition to the late filing fee.

Categories of ITR

The Income Tax Department notifies different ITR forms each year to suit various categories of taxpayers. Selecting the correct form is essential, as filing in an incorrect form may render the return defective. For FY 2024–25 (AY 2025–26), the following forms are applicable to non-audit taxpayers, including individuals and small entities:

ITR-1 (Sahaj) – For Salaried Individuals

A salaried individual, as per the Income Tax Department, is a taxpayer whose income is earned from an employer in the form of salary, wages, allowances, perquisites, or pension and is chargeable under the head “Income from Salary.”

Who Can Use ITR-1?

ITR-1 can be used by individuals who:

- Are Resident Individuals (Not Ordinarily Resident)

- Have a total income up to ₹50 lakh

- Have income from: Salary or Pension, One House Property, Other Sources (bank interest, family pension), Agricultural income up to ₹5,000

Who Cannot Use ITR-1?

ITR-1 cannot be used by individuals who:

- Have total income exceeding ₹50 lakh

- Have income from more than one house property

- Have income under the head Capital Gains (including short-term gains or long-term gains u/s 112A exceeding ₹1.25 lakh)

- Are Directors in a company

- Have held any unlisted equity shares at any time during the previous year

- Have any asset (including financial interest in any entity) located outside India

- Have signing authority in any account located outside India

- Have income from any source outside India

- Have income from business or profession

- Have deferred tax on ESOPs(Employee Stock Options)

- Have income on which tax has been deducted u/s 194N

- Have any brought forward loss or loss to be carried forward under any head of income

ITR-2 – For Individuals/HUFs (No Business/Profession Income)

Individuals are natural persons who earn income from salary, pension, house property, capital gains, business/profession, or other sources and are taxed in their personal capacity.

HUFs (Hindu Undivided Families) are separate entities under income tax law consisting of all persons lineally descended from a common ancestor, including their wives and unmarried daughters. An HUF can earn income from property, business, or other sources, and it is taxed as a distinct “person” under the Income Tax Act.

Who Can File:

- Individuals and Hindu Undivided Families (HUFs) who are not eligible to file ITR-1 (Sahaj)

- Taxpayers not having income from “Profits and Gains of Business or Profession”

- Taxpayers not having income in the nature of interest, salary, bonus, commission, or remuneration received from a partnership firm

- Cases where the income of another person (such as spouse, minor child, etc.) is required to be clubbed with the taxpayer’s income, provided the income to be clubbed falls under the eligible categories for ITR-2

Who Cannot File:

- Individuals and Hindu Undivided Families (HUFs) whose total income for the year includes income from “Profits and Gains of Business or Profession”, and

- Income is in the nature of interest, salary, bonus, commission, or remuneration received from a partnership firm

ITR-3 – For Individuals & HUFs With Business/Profession Income

Who Can File:

- Individuals and Hindu Undivided Families (HUFs) having income under the head Profits and Gains of Business or Profession

- Individuals and HUFs whose income is chargeable to tax under the head “Profits and gains of business or profession” received from a partnership firm.

Who Cannot File:

- Those eligible for ITR-1, ITR-2, or ITR-4

ITR-4 (Sugam) – For Presumptive Income

Presumptive income, as per the Income Tax Department of India, refers to income that is calculated on a presumptive basis instead of maintaining detailed books of accounts.

Under the presumptive taxation scheme, the Income Tax Act allows certain taxpayers (small businesses, professionals, and transporters) to declare income at a prescribed rate of turnover or receipts, without the need to maintain regular accounts or undergo audits.

Who Can File:

ITR-4 can be filed by:

- Individuals, Hindu Undivided Families (HUFs), and Firms (other than LLPs) who are residents

- Those who have income from business or profession calculated on a presumptive basis

- Along with business income, they can also have salary or pension, income from one house property, income from other sources (such as bank interest, family pension, or dividend), and agricultural income up to ₹5,000

Who Cannot File:

You cannot use ITR-4 if you:

- Earn more than ₹50 lakh in a year

- Are a Director in a company

- Own more than one house property

- Have capital gains (profit from selling shares, property, etc.), including long-term gains above ₹1.25 lakh under Section 112A

- Have held unlisted company shares at any time during the year

- Own assets outside India or have foreign income

- Have authority to operate a bank account outside India

- Have deferred tax on ESOPs

- Have any brought forward loss or loss to be carried forward under any head of income

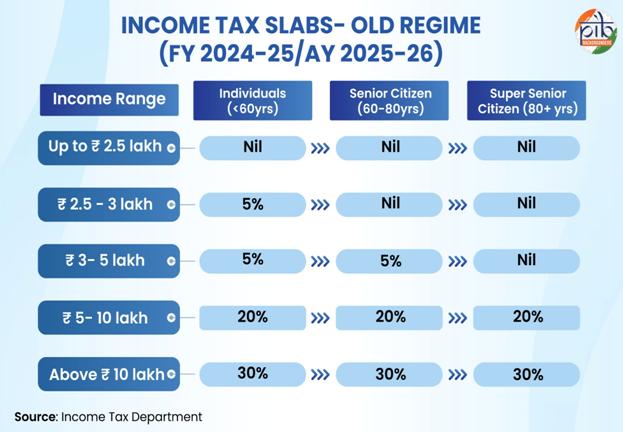

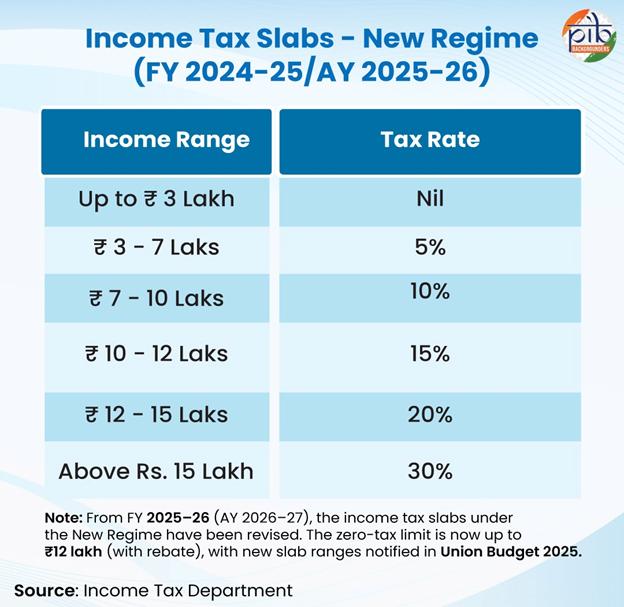

Old vs New Tax Regime (For FY 2024-25 / AY 2025-26)

When filing an Income Tax Return (ITR), taxpayers are required to choose between the Old Tax Regime and the New Tax Regime. This choice determines how income will be taxed and whether deductions and exemptions can be claimed.

The Old Regime continues the traditional system of higher tax rates but provides a wide range of exemptions and deductions under the Income Tax Act, making it more suitable for individuals who plan their finances through investments and savings. In contrast, the New Regime, introduced in the Union Budget 2020, aims to simplify taxation by offering reduced slab rates with minimal exemptions. It is especially helpful for taxpayers who prefer a straightforward system without the need for detailed tax planning or documentation. From FY 2023–24 onwards, the New Regime has been made the default option, though taxpayers retain the flexibility to opt for whichever system benefits them more.

|

Feature

|

Old Tax Regime

|

New Tax Regime

|

|

Tax Rates

|

Higher slab rates

|

Lower slab rates

|

|

Exemptions & Deductions

|

Standard Deduction ₹50,000, plus a wide range of exemptions like investments, insurance, home loan interest etc.

|

Limited (Standard Deduction ₹75,000, Employer’s NPS contribution, Family pension deduction)

|

|

Investments (80C)

|

Investments in PF, LIC, ELSS, PPF, etc. – up to ₹1.5 lakh

|

-

|

|

Medical Insurance (80D)

|

Medical Insurance – up to ₹25,000 (₹50,000 for senior citizens)

|

-

|

|

Rebate

|

Taxable income up to ₹5 lakh → Nil tax

|

Taxable income up to ₹7 lakh → Nil tax

|

|

Default Option

|

Optional (must be chosen by taxpayer)

|

Default regime from FY 2023–24; option to switch to Old Regime if beneficial

|

How to File Your ITR

- Log in at incometax.gov.in using PAN/Aadhaar & password

- Go to → e-File > Income Tax Return > File Income Tax Return

- Select AY 2025–26

- Choose your applicable form

- Review pre-filled details (salary, TDS, bank interest)

- Add missing income/deductions & select tax regime (Old/New)

- Submit return

Growth in ITR Filing

Growth: Over 25% increase in ITR filings between AY 2022–23 and AY 2024–25

|

As per data released byCBDT, ITR filings have shown consistent growth over the years, reflecting rising compliance and widening of the tax base. For AY 2024–25, a record 7.28 crore ITRs were filed up to 31 July 2024, compared to 6.77 crore in AY 2023–24, registering a 7.5% year-on-year growth.

Out of the total filings, 72% of taxpayers (5.27 crore) opted for the New Tax Regime, while 28% (2.01 crore) continued with the Old Regime. The e-filing portal also handled record activity on the due date (31 July 2024), with 69.92 lakh returns filed in a single day. Importantly, the tax base continued to expand, with 58.57 lakh first-time filers joining in AY 2024–25.

Conclusion

The extension of the due date for filing Income Tax Returns for FY 2024–25 (AY 2025–26) to 15 September 2025 provides additional time for taxpayers to complete their compliance obligations. Data from CBDT shows that ITR filings have recorded steady growth, with 7.28 crore returns filed up to 31 July 2024, reflecting both increased digital adoption and widening of the tax base. The growing participation of first-time filers, alongside the majority opting for the New Tax Regime, indicates a shift towards simplified compliance and greater formalisation of the economy.

Timely and accurate filing of returns continues to play an important role in strengthening financial credibility for individuals and in supporting effective governance for the country. Rising ITR filings demonstrate the success of government initiatives aimed at ease of compliance, transparency, and expanding taxpayer participation in India’s economic growth.

Reference:

Income Tax Department, Ministry of Finance

PIB

Download in PDF

***

SK/M

(Backgrounder ID: 155163)

Visitor Counter : 1

Provide suggestions / comments

Read this release in:

Hindi