Economy

RBI Issues June 2025 Monetary Policy Update

Posted On: 06 JUN 2025 4:48PM

RBI has announced its latest Monetary Policy today, that is 6th of June 2025, following the 55th meeting of its Monetary Policy Committee over 4th-6th June 2025. The major decisions include:

Repo Rate Reduction

- Policy repo rate is being reduced by 50 basis points (bps) to 5.50 per cent with immediate effect.

- There will be consequent adjustment of the Standing Deposit Facility (SDF) rate under the Liquidity Adjustment Facility (LAF) to 5.25 per cent and of the Marginal Standing Facility (MSF) rate and the Bank Rate to 5.75 per cent.

With this decision RBI hopes to fulfil the objective of achieving the medium-term target for consumer price index (CPI) inflation of 4 per cent within a band of +/- 2 per cent, while stepping up growth momentum.

Growth Outlook

The policy notes and takes into consideration various positive and negative factors and prevailing conditions that may impact the economy in the coming months.

- The report notes both positive and negative Even though uncertainty around the global economic outlook has come down a little, it remains high enough for multilateral agencies to revise global growth and trade projections downwards.

- Market volatility has eased in the recent period with equity markets staging a recovery, dollar index and crude oil softening though gold prices remain high.

- The National Statistical Office (NSO) vide its estimates of May 30, 2025, has shown real GDP growth in Q4:2024-25 at 7.4 per cent as against 6.4 per cent in Q3. Real Gross Value Added (GVA) rose by 6.8 per cent in Q4:2024-25. For 2024-25, real GDP growth was placed at 6.5 per cent, while real GVA recorded a growth of 6.4 per cent.

- Economic activity continues to maintain the momentum in 2025-26, supported by private consumption and traction in fixed capital formation.

- Investment activity is expected to improve in light of higher capacity utilization, improving balance sheets of financial and non-financial corporates, and government’s capital expenditure push

- Trade policy uncertainty continues to weigh on exports prospects, however the conclusion of free trade agreement (FTA) with the United Kingdom and progress with other countries is supportive of trade activity.

- Agriculture prospects remain bright on the back of an above normal south- west monsoon forecast and resilient allied activities.

- Services sector is expected to maintain its momentum.

- However, Spillovers emanating from protracted geopolitical tensions, and global trade and weather-related uncertainties pose downside risks to growth.

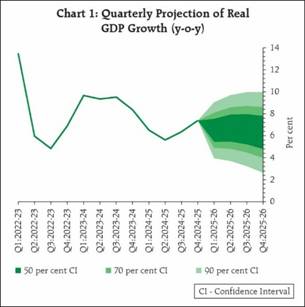

Taking into consideration the above factors the policy projects Real GDP growth for 2025-26 is projected at 6.5 per cent, with Q1 at 6.5 per cent, Q2 at 6.7 per cent, Q3 at 6.6 per cent, and Q4 at 6.3 per cent (Chart 1). The risks are evenly balanced.

Inflation Outlook

The policy notes that CPI headline inflation continued its declining trajectory in March and April, with headline CPI inflation moderating to a nearly six-year low of 3.2 per cent (year-on- year) in April 2025. Food inflation recorded the sixth consecutive monthly decline. Core inflation remained largely steady and contained during March-April.

- The outlook for inflation points towards benign prices across major constituents.

- Record wheat production and higher production of key pulses in the Rabi crop season, and expected above normal monsoon along with its early onset augurs well for Kharif crop prospects should ensure adequate supply of key food items. Reflecting this, inflation expectations are showing a moderating trend, more so for the rural households.

- Most projections point towards continued moderation in the prices of key commodities, including crude oil.

- Notwithstanding these favourable prognoses, we need to remain watchful of weather-related uncertainties and still evolving tariff related concerns with their attendant impact on global commodity prices.

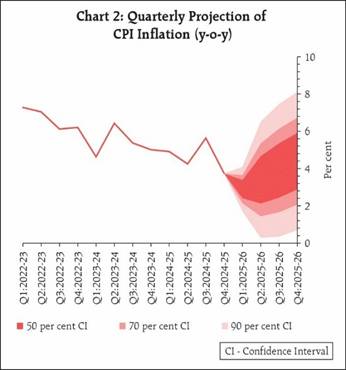

Taking the above factors into consideration the policy projects CPI inflation for the financial year 2025-26 at 3.7 per cent, with Q1 at 2.9 per cent; Q2 at 3.4 per cent; Q3 at 3.9 per cent; and Q4 at 4.4 per cent (Chart 2). The risks are evenly balanced.

Background

The monetary policy of a country includes actions that it takes to control money supply and credit conditions in the economy. The objective is to achieve price stability and support economic growth. In India, this function is assigned to the Reserve Bank of India in terms of The RBI Act,1934 (as amended in 2016). The Act provides for setting up of a six-member Monetary Policy Committee of which three are from within RBI and three members are nominated by the Government of India.

There are several direct and indirect tools for implementing monetary policy. These include:

- Repo Rate: The Repo Rate is the interest rate at which the Reserve Bank of India (RBI) loans money to commercial banks. More specifically, it is the interest rate at which the Reserve Bank provides liquidity under the liquidity adjustment facility (LAF) to all LAF participants against the collateral of government and other approved securities.

- Standing Deposit Facility (SDF) Rate: The rate at which the Reserve Bank accepts uncollateralised deposits, on an overnight basis, from all LAF participants. The SDF is also a financial stability tool in addition to its role in liquidity management. The SDF rate is placed at 25 basis points below the policy repo rate. With introduction of SDF in April 2022, the SDF rate replaced the fixed reverse repo rate as the floor of the LAF corridor.

- Marginal Standing Facility (MSF) Rate: The penal rate at which banks can borrow, on an overnight basis, from the Reserve Bank by dipping into their Statutory Liquidity Ratio (SLR) portfolio up to a predefined limit (2 per cent). This provides a safety valve against unanticipated liquidity shocks to the banking system. The MSF rate is placed at 25 basis points above the policy repo rate.

- Liquidity Adjustment Facility (LAF): The LAF refers to the Reserve Bank's operations through which it injects/absorbs liquidity into/from the banking system. It consists of overnight as well as term repo/reverse repos (fixed as well as variable rates), SDF and MSF. Apart from LAF, instruments of liquidity management include outright open market operations (OMOs), forex swaps and market stabilisation scheme (MSS).

- LAF Corridor: The LAF corridor has the marginal standing facility (MSF) rate as its upper bound (ceiling) and the standing deposit facility (SDF) rate as the lower bound (floor), with the policy repo rate in the middle of the corridor.

- Main Liquidity Management Tool: A 14-day term repo/reverse repo auction operation at a variable rate conducted to coincide with the cash reserve ratio (CRR) maintenance cycle is the main liquidity management tool for managing frictional liquidity requirements.

- Fine Tuning Operations: The main liquidity operation is supported by fine-tuning operations, overnight and/or longer tenor, to tide over any unanticipated liquidity changes during the reserve maintenance period. In addition, the Reserve Bank conducts, if needed, longer-term variable rate repo/reverse repo auctions of more than 14 days.

- Reverse Repo Rate: The interest rate at which the Reserve Bank absorbs liquidity from banks against the collateral of eligible government securities under the LAF. Following the introduction of SDF, the fixed rate reverse repo operations will be at the discretion of the RBI for purposes specified from time to time.

- Bank Rate: The rate at which the Reserve Bank is ready to buy or rediscount bills of exchange or other commercial papers. The Bank Rate acts as the penal rate charged on banks for shortfalls in meeting their reserve requirements (cash reserve ratio and statutory liquidity ratio). The Bank Rate is published under Section 49 of the RBI Act, 1934. This rate has been aligned with the MSF rate and, changes automatically as and when the MSF rate changes alongside policy repo rate changes.

- Cash Reserve Ratio (CRR): The average daily balance that a bank is required to maintain with the Reserve Bank as a per cent of its net demand and time liabilities (NDTL) as on the last Friday of the second preceding fortnight that the Reserve Bank may notify from time to time in the Official Gazette.

- Statutory Liquidity Ratio (SLR): Every bank shall maintain in India assets, the value of which shall not be less than such percentage of the total of its demand and time liabilities in India as on the last Friday of the second preceding fortnight, as the Reserve Bank may, by notification in the Official Gazette, specify from time to time and such assets shall be maintained as may be specified in such notification (typically in unencumbered government securities, cash and gold).

- Open Market Operations (OMOs): These include outright purchase/sale of government securities by the Reserve Bank for injection/absorption of durable liquidity in the banking system.

The RBI Monetary Policy contains the following elements:

a) Explanation of inflation dynamics and the near-term inflation outlook;

b) Projections of inflation and growth and the balance of risks

c) An assessment of the state of the economy

d) An updated review of the operating procedure of monetary policy; and

e) An assessment of projection performance.

References:

- https://www.rbi.org.in/Scripts/BS_PressReleaseDisplay.aspx?prid=60605

- https://www.rbi.org.in/Scripts/BS_PressReleaseDisplay.aspx?prid=60604

- https://www.rbi.org.in/scripts/FS_Overview.aspx?fn=2752

- https://www.rbi.org.in/scripts/FS_Overview.aspx?fn=2752

Click here to download PDF

*****

Santosh Kumar/ Neeta Prasad/ Saurabh Kalia

(Backgrounder ID: 154573)

Visitor Counter : 503