Finance Minister exhorts PSBs to focus more on branch based banking with customer connect

Finance Minister unveils EASE Roadmap for Banking of the Future

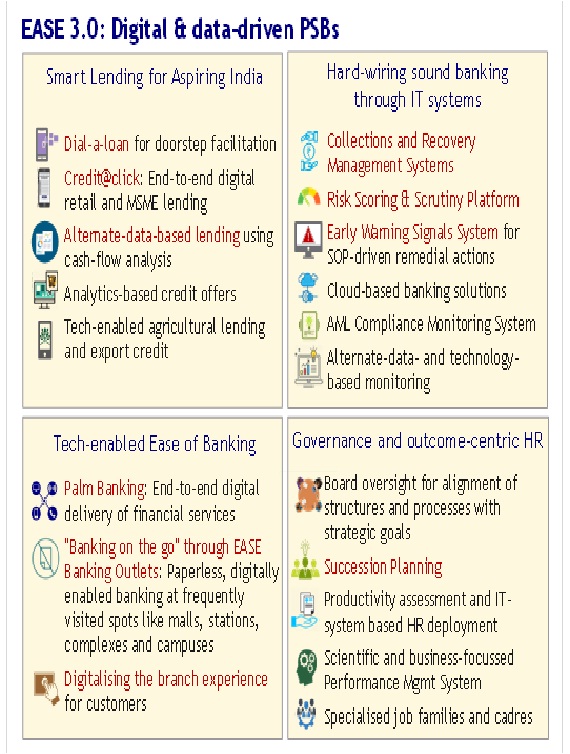

EASE 3.0 Reforms Agenda commits Public Sector Banks to Tech-Enabled Banking

PSBs to offer Credit@click, Dial-a-loan, and banking-on-the-go EASE Outlets

Union Minister for Finance & Corporate Affairs Smt. Nirmala Sitharaman today unveiled EASE 3.0, the Public Sector Bank (PSB) Reforms Agenda 2020-21 for smart, tech-enabled banking, and the PSB EASE Reforms Annual Report 2019-20 here today.

Finance Minister Smt. Sitharaman exhorted Public Sector Banks (PSBs) to have one-to-one interface with their customers through branch based banking and not rely so much on credit ratings agencies. She said that banks need to connect with their customers by leveraging technology but not exclusively only through the interface of technology. In her address on the occasion, the Finance Minister asked the bankers to focus more at the grassroot level.

Smt. Sitharaman further exhorted banks to be friendlier to its customers by using local language in bank branch. She said that PSBs have played a great role in enabling financial inclusion in the country.

EASE 3.0 seeks to enhance ease of banking in all customer experiences, using technology, Finance Minister Smt. Nirmala SitharamanFinTech, alternate data and analytics. Dial-a-loan for doorstep loan facilitation, Credit@click for end-to-end digitalised lending, on-the-spot EASE Banking Outlets at well-frequented places like malls and stations, palm banking, digitalised branch experience, analytics-based instant credit offers, cash-flow-based credit and tech-enabled agriculture lending are part of a wide array of tech-enabled ease enhancements that PSBs would effect during FY2020-21.

Minister of State for Finance and Corporate Affairs Anurag Thakur was the guest of honour for the event. Finance Secretary Rajiv Kumar, Secretary Designate cum Special Secretary (Financial Services) Debashish Panda and Chairman IBA, Rajnish Kumar also graced the unveiling event.

Preview of Banking of the Future

At the launch function organised by Indian Banks’ Association at Delhi, individual PSBs gave a preview of the array of tech-enabled services that are in the pipeline or have been piloted and will be scaled up over the coming year across PSBs. UCO Bank unveiled its plans for customers to obtain via app, portal or call centre, Doorstep Banking Services offered collectively by PSBs as “PSB Alliance”, for services such as pick-up of cheques and income-tax exemption certificates and delivery of income-tax challan, drafts and account statements in major cities across India. State Bank of India showcased Shishu e-Mudra app-based lending for instant sanction of working capital up to Rs. 50,000 to existing small business customers of the bank and the bank announced its plan to scale up sanctioning through the app to Rs. 1 lakh in branch-assist mode. Union Bank of India gave a preview of its app for end-to-end digitalised lending to MSMEs of up to Rs. 50 crore, which it proposes to roll out during the coming year. Bank of Baroda showcased its tablet-based Tab Banking services for doorstep account-opening, including in villages and for migrant labourers in industrial units, and has created capacity for opening about 10,000 accounts per day. Bank of Baroda also gave a preview of its tab-based doorstep loan application, disbursement and collection for informal enterprises in partnership with NBFCs, including in rural areas. Syndicate Bank presented micro ATM and tablet based doorstep micro-financing of women entrepreneurs. State Bank of India also presented one-stop online agriculture ecosystem for meeting farmers’ needs in the form of app-based YONO Krishi, which enables credit including agricultural gold loan, estimation and purchase of agricultural inputs, and information needed for agricultural operations. The bank also announced its plan to introduce SAFAL for pre-approved agricultural loan along with multipurpose insurance cover.

The PSB EASE Reforms journey

PSB Reforms EASE Agenda is a common reform agenda for PSBs aimed at institutionalizing clean and smart banking. It was launched in January 2018, and the subsequent edition of the program ― EASE 2.0 built on the foundation laid in EASE 1.0 and furthered the progress on reforms. Reform Action Points in EASE 2.0 aimed at making the reforms journey irreversible, strengthening processes and systems, and driving outcomes. Public Sector Banks have shown significant improvement in the Action Points of the EASE Reforms Agenda since its introduction.

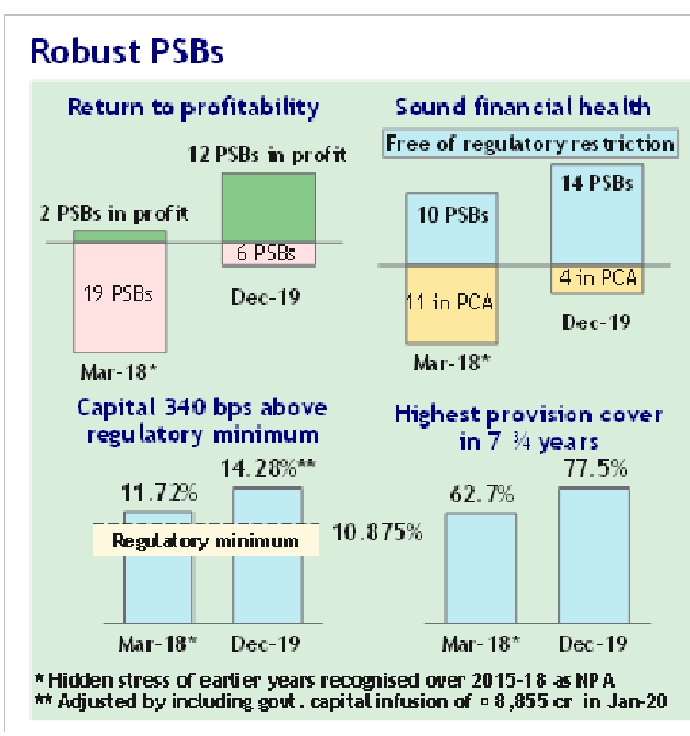

Following the completion of recognition of legacy stress as NPA, PSBs have returned to profitability with sound financial health and institutionalised systems to prevent the recurrence of past weaknesses. The improved financial health of PSBs reflects in many parameters—

Gross NPAs reduced from Rs 8.96 lakh crore (14.6%) in March-2018 to Rs 7.17 lakh crore (11.3%) in December-2019;

Gross NPAs reduced from Rs 8.96 lakh crore (14.6%) in March-2018 to Rs 7.17 lakh crore (11.3%) in December-2019;- A sharp decline in fraud occurrence from 0.65% of advances during FY10-FY14 to 0.20% in FY18-FY20; due to fraud prevention reforms and proactive checking of legacy NPA

- Record recovery of Rs 2.04 lakh crore in FY19-9MFY20 driven by newly setup dedicated stressed account management verticals in PSBs that have recovered Rs 1.21 lakh crore in the same period;

- Number of PSBs under PCA down to four;

- 12 PSBs reporting profits in 9MFY20;

- CRAR 340 bps above the regulatory minimum; and

- The highest provision coverage ratio of 77.5% in nearly eight years.

EASE 3.0 — Smart, Tech-enabled Banking for Aspiring India

Over the last five years, PSBs have not only cleaned up legacy stress and addressed underlying systemic weaknesses but have emerged stronger as a result of comprehensive and institutionalized EASE reforms. EASE 3.0 sets the agenda and roadmap for FY21 for their transformation into digital and data-driven NextGen Banking of the Future for an aspiring India.

With EASE 1.0 and 2.0 laying a firm foundation of robust banking and institutionalised systems, PSBs are set to transform into digital- and data-driven NextGen banks. EASE 3.0 emphasizes on the use of digital, analytics & AI, FinTech partnerships across customer service, convenient banking, end-to-end digitalised processes for loan sourcing and processing, analytics-driven risk management as well as decision support systems for HR.

Key Reform Action Points in EASE 3.0 include:

- Dial-a-loan: Digitally-enabled doorstep facilitation for initiation of retail and MSME loans. Customers will have the facility to register loan requests through digitally-enabled channels

- Customer-need driven credit offers by larger PSBs to existing customers through analytics, e.g., for EMI on expenses like holidays/school-fees/jewellery/consumer durables, home loan takeovers, loan-against-property post home loan closure, working capital enhancement based on sales jump

- Partnerships with FinTechs and E-commerce companies for customer-need driven credit offers

- Credit@click: End-to-end digitalised, time-bound retail and MSME lending by larger PSBs, leveraging Account Aggregators, FinTechs and PSBloansin59minutes.com

- Cash-flow-based MSME credit by larger PSBs, using FinTech, Account Aggregator and other third-party data and transactions-based underwriting models

- Tech-enabled agriculture lending

- Palm banking: End-to-end digitalised delivery of a full bouquet of financial services in regional languages and with industry-best service quality

- EASE Banking Outlets: On-the-spot banking at frequently visited places such as train stations, bus stands, malls, hospitals, etc. through paperless and digitally-enabled banking outlets and kiosks

PSBs have already started taking steps based on the reforms agenda. During the event, several digitally-enabled banking solutions, such as tablet-banking, digitally-driven agriculture lending, paperless and digitally-enabled EASE bank outlets, were demonstrated by the PSBs. Progress of PSBs will continue to be tracked on metrics linked to Reform Action Points, and their progress will be published through a quarterly index.

Performance of PSB on EASE 2.0 Index

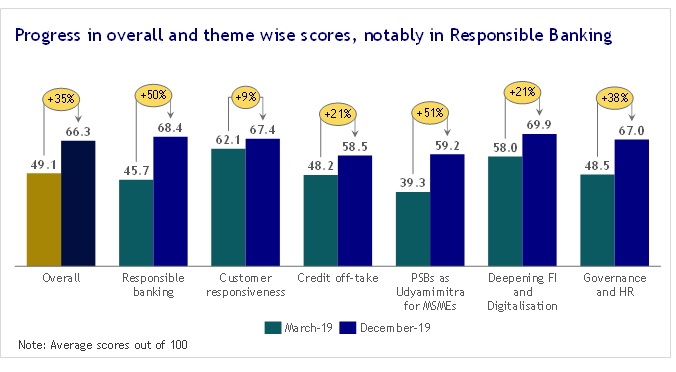

PSBs have shown a healthy trajectory in their performance over three quarters since the launch of EASE 2.0 Reforms Agenda. The overall score of PSBs increased by 35% between March-2019 and December-2019, with the average EASE index score improving from 49.1 to 66.3 out of 100. Significant progress is seen across six themes of the Reforms Agenda, with the highest improvement seen in the themes of ‘Responsible Banking’ and ‘PSBs as Udyamimitra for MSMEs’.

PSBs have shown a healthy trajectory in their performance over three quarters since the launch of EASE 2.0 Reforms Agenda. The overall score of PSBs increased by 35% between March-2019 and December-2019, with the average EASE index score improving from 49.1 to 66.3 out of 100. Significant progress is seen across six themes of the Reforms Agenda, with the highest improvement seen in the themes of ‘Responsible Banking’ and ‘PSBs as Udyamimitra for MSMEs’.

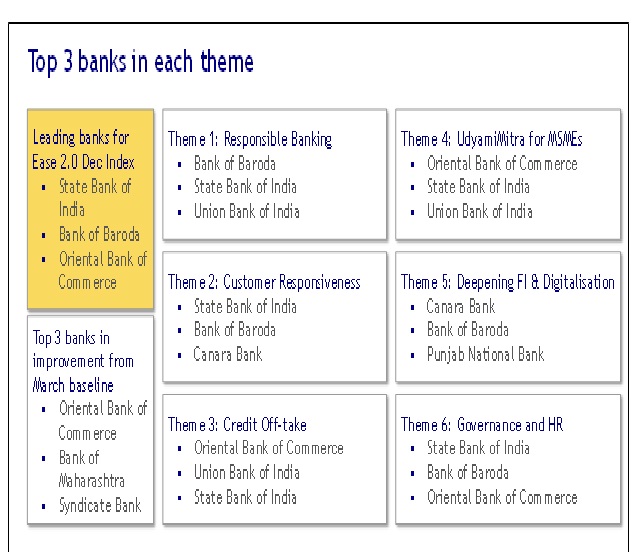

State Bank of India, Bank of Baroda and Oriental Bank of Commerce are the front-runners for the best performing banks. The final EASE 2.0 index will be published after declaration of bank results for the financial year.

State Bank of India, Bank of Baroda and Oriental Bank of Commerce are the front-runners for the best performing banks. The final EASE 2.0 index will be published after declaration of bank results for the financial year.

Major Reform achievements over March 2018 to December 2019

- Significant improvement in customer outreach through dedicated marketing force and external partnerships. The number of dedicated marketing employees has increased from 8,920 to 17,617

- Turnaround time for loans reduced by 67% from the average of nearly 30 days to nearly 10 days

- 80% of PSB customers now have access to 35+ services on mobile/ Internet banking, 23 services on call center. The availability of services has nearly doubled over last 18 months.

- Improvement in the availability of regional languages in call-centers has increased four-fold

- Complaint redressal turnaround time reduced from the average of 9 days to 6 days

- 20 branch-equivalent services made available by PSBs through Bank Mitras

- For prudential lending, PSBs are now systematically keeping watch on adherence to risk-based pricing, and cases with deviation have reduced from 59% to 23%, and have put in place data-driven risk-scoring for appraisal of high-value loans that factors in group-entities.

- Most PSBs have deployed IT-based EWS systems leveraging third-party data, which have enabled early, time-bound action in stressed accounts. Monitoring has also been strengthened by deploying Agencies for Specialised Monitoring, and proactively monitoring listed entities based on published financials. Slippage into NPA has reduced from 3.90 lakh crore in 12-months ending March-18 to 1.88 lakh crore in 12-months ending December-19.

- PSBs have adopted digital platforms such as online OTS, e-Bक्रय, e-DRT for expedited recovery. 87% of one-time settlement (OTS) cases are now tracked through dedicated IT systems.

- PSBs have adopted new ways of credit. 63% of all PSB inland bills are now discounted through online TReDS

- 40% YoY growth in the quarterly value of loans disbursed through psbloansin59minutes.com (Dec-20)

- The Government has introduced several governance reforms. The governance reforms include arm’s length selection of top bank management through Banks Board Bureau, introduction of non-executive chairpersons, broader talent pool for such selections, empowered bank Boards, strengthening of the Board committees system, enhancing the effectiveness of non-official directors, and leadership development and succession planning for the top two levels below the Board. In larger PSBs, Executive Director strength has been increased, and Boards are empowered to introduce CGM level for increased business.

Like in the previous year, progress made by PSBs was tracked quarterly through a published EASE Reforms Index leading up to the annual review. In addition to the inclusion of the EASE Reforms Index in the evaluation of Whole Time Directors of PSBs, it has now been made part of the annual appraisal of PSB leadership up to two levels below the Whole Time Directors.

The Index measures the performance of each PSB on 100+ objective metrics across six themes. It provides all PSBs a comparative evaluation showing where banks stand vis-à-vis benchmarks and peers on the Reforms Agenda. The Index follows a fully transparent scoring methodology, which enables banks to identify precisely their strengths as well as areas for improvement. The goal is to continue driving change by spurring healthy competition among PSBs and also by encouraging them to learn from each other.

****

RM/KMN